The NFIB Research Foundation has collected Small Business Economic Trends data with quarterly surveys since the 4th quarter of 1973 and monthly surveys since 1986. Survey respondents are drawn from NFIB’s membership. The report is released on the second Tuesday of each month. This survey was conducted in April 2024.

Small Business Optimism Index

April 2024 Report:

Inflation Continues to Hinder Small Business Operations

NFIB’s Small Business Optimism Index rose by 1.2 points in April to 89.7, marking the first increase of this year but the 28th consecutive month below the 50-year average of 98. Twenty-two percent of owners reported that inflation was their single most important problem in their business, down three points from March but still the number one problem for small business owners.

“Cost pressures remain the top issue for small business owners, including historically high levels of owners raising compensation to keep and attract employees,” said Bill Dunkelberg, NFIB Chief Economist. “Overall, small business owners remain historically very pessimistic as they continue to navigate these challenges. Owners are dealing with a rising level of uncertainty but will continue to do what they do best – serve their customers.”

Key findings include:

- The net percent of owners who expect real sales to be higher rose six points from March to a net negative 12% (seasonally adjusted).

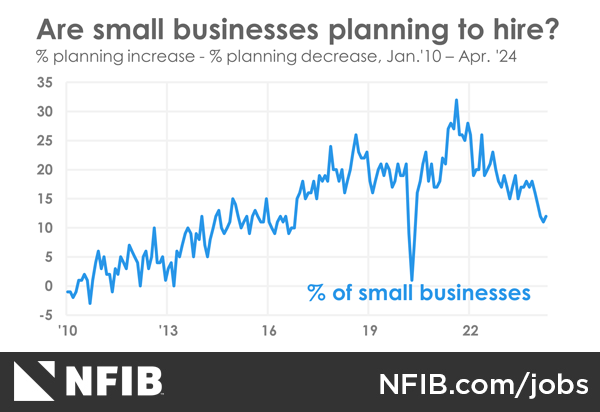

- A seasonally adjusted net 12% of owners reported planning to create new jobs in the next three months, up one point from March’s lowest level since May 2020.

- A net 26% (seasonally adjusted) of owners plan price hikes in April, down seven points and the lowest reading since April of last year.

- Forty percent (seasonally adjusted) of all owners reported job openings they could not fill in the current period, up three points from March, which was the lowest reading since January 2021.

- The net percent of owners raising average selling prices fell three points from March to a net 25% seasonally adjusted.

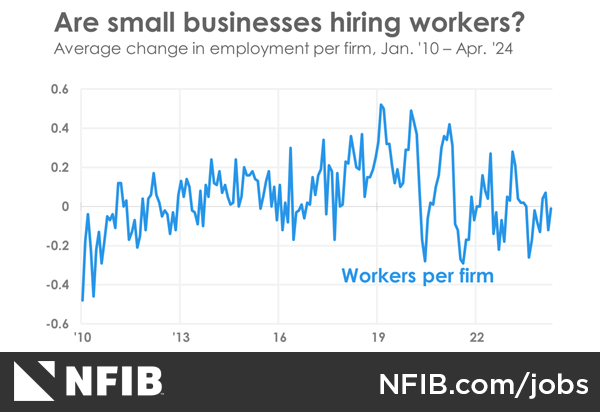

As reported in NFIB’s monthly jobs report, 56% of owners reported hiring or trying to hire in April, and of those hiring or trying to hire, 91% of owners reported few or no qualified applicants for the positions they were trying to fill.

Fifty-six percent of owners reported capital outlays in the last six months, unchanged from March. Of those making expenditures, 38% reported spending on new equipment, 24% acquired vehicles, and 16% improved or expanded facilities. Eleven percent spent money on new fixtures and furniture and 6% acquired new buildings or land for expansion. Twenty-two percent (seasonally adjusted) plan capital outlays in the next few months.

A net negative 13% of all owners (seasonally adjusted) reported higher nominal sales in the past three months. The net percent of owners expecting higher real sales volumes rose six points to a net negative 12% (seasonally adjusted).

The net percent of owners reporting inventory gains rose one point to a net negative 6%. Not seasonally adjusted, 12% reported increases in stocks and 17% reported reductions. A net negative 4% (seasonally adjusted) of owners viewed current inventory stocks as “too low” in April. A net negative 6% of owners plan inventory investment in the coming months.

The net percent of owners raising average selling prices fell three points from March to a net 25% seasonally adjusted. Twenty-two percent of owners reported that inflation was their single most important problem in operating their business, down three points from March.

Thirteen percent of owners reported lower average selling prices and 41% reported higher average prices. Price hikes were the most frequent in the finance (54% higher, 7% lower), retail (49% higher, 8% lower), construction (48% higher, 7% lower), manufacturing (40% higher, 7% lower), and wholesale (40% higher, 10% lower) sectors. Seasonally adjusted, a net 26% of owners plan price hikes in April.

Seasonally adjusted, a net 38% reported raising compensation in April. A net 21% (seasonally adjusted) of owners plan to raise compensation in the next three months, unchanged from March.

Eleven percent of owners cited labor costs as their top business problem, up one point from March and two points below the highest reading of 13% reached in December 2021. Nineteen percent said that labor quality was their top business problem, remaining behind inflation as the number one issue.

The frequency of reports of positive profit trends was a net negative 27% (seasonally adjusted), two points better than March but still a very poor reading. Among owners reporting lower profits, 33% blamed weaker sales, 14% blamed the rise in the cost of materials, 13% cited usual seasonal change, and 12% cited labor costs. For owners reporting higher profits, 43% credited sales volumes, 26% cited usual seasonal change, and 11% cited higher selling prices.

Three percent of owners reported that all their borrowing needs were not satisfied, up one point from March. Twenty-eight percent of owners reported all credit needs met and 60% said they were not interested in a loan. A net 8% reported their last loan was harder to get than in previous attempts.

Four percent of owners reported that financing was their top business problem in April. A net 21% of owners reported paying a higher rate on their most recent loan, up four points from March.

The NFIB Research Center has collected Small Business Economic Trends data with quarterly surveys since the fourth quarter of 1973 and monthly surveys since 1986. Survey respondents are randomly drawn from NFIB’s membership. The report is released on the second Tuesday of each month. This survey was conducted in April 2024.

LABOR MARKETS

Forty percent (seasonally adjusted) of all owners reported job openings they could not fill in the current period, up 3 points from March’s lowest reading since January 2021. Thirty-four percent have openings for skilled workers (up 3 points) and 18 percent have openings for unskilled labor (up 4 points). The difficulty in filling open positions is particularly acute in the transportation, construction, and wholesale sectors. Job openings in construction were up 11 points from last month and over half of the firms (55%) have a job opening they can’t fill. Openings were the lowest in the agriculture and finance sectors. Owners’ plans to hire reversed trend, with a seasonally adjusted net 12 percent planning to create new jobs in the next three months, up 1 point from March’s lowest level since May 2020. Overall, 56 percent reported hiring or trying to hire in April, unchanged for the third consecutive month. Fifty-one percent (91 percent of those hiring or trying to hire) of owners reported few or no qualified applicants for the positions they were trying to fill (up 3 points). Twenty-eight percent of owners reported few qualified applicants for their open positions (down 1 point) and 23 percent reported none (up 4 points). Reports of labor quality as the single most important problem for business owners rose 1 point to 19 percent. However, labor quality as small business owners’ top problem has eased considerably over the last two quarters. Labor cost reported as the single most important problem for business owners increased 1 point to 11 percent, only 2 points below the highest reading of 13 percent reached in December 2021.

Click images to view

CAPITAL SPENDING

Fifty-six percent reported capital outlays in the last six months, unchanged from March. A recovery in investment is needed to support stronger productivity, but this is unlikely to occur while interest rates remain high, and more owners anticipate slower sales. Long term, the worker shortage has given firms an incentive to invest in labor saving technology. But, overall, capital spending is sluggish and not yet back to pre-pandemic levels. Of those making expenditures, 38 percent reported spending on new equipment (unchanged), 24 percent acquired vehicles (unchanged), and 16 percent improved or expanded facilities (down 1 point). Eleven percent spent money on new fixtures and furniture (up 1 point) and 6 percent acquired new buildings or land for expansion (up 1 point). Twenty-two percent (seasonally adjusted) plan capital outlays in the next few months, up 2 points from March.

INFLATION

The net percent of owners raising average selling prices fell 3 points from March to a net 25 percent seasonally adjusted. Twenty-two percent of owners reported that inflation was their single most important problem in operating their business (higher input and labor costs), down 3 points from March. Unadjusted, 13 percent (unchanged) reported lower average selling prices and 41 percent (down 2 points) reported higher average prices. Price hikes were most frequent in the finance (54 percent higher, 7 percent lower), retail (49 percent higher, 8 percent lower), construction (48 percent higher, 7 percent lower), manufacturing (40 percent higher, 7 percent lower), and wholesale (40 percent higher, 10 percent lower) sectors. Seasonally adjusted, a net 26 percent plan price hikes in April (down 7 points). This is the lowest reading since April of last year.

CREDIT MARKETS

Three percent of owners reported that all their borrowing needs were not satisfied, up 1 point from March. Twenty-eight percent reported all credit needs met (up 1 point) and 60 percent said they were not interested in a loan (up 1 point). A net 8 percent reported their last loan was harder to get than in previous attempts (unchanged). Four percent reported that financing was their top business problem in April (unchanged). A net 21 percent of owners reported paying a higher rate on their most recent loan, up 4 points from March. The average rate paid on short maturity loans was 9.3 percent, down by half a point from last month. Thirty-one percent of all owners reported borrowing on a regular basis, up 3 points from March.

COMPENSATION AND EARNINGS

Seasonally adjusted, a net 38 percent reported raising compensation, unchanged from March. A seasonally adjusted net 21 percent plan to raise compensation in the next three months, unchanged from March. Eleven percent cited labor costs as their top business problem, up 1 point from March and only 2 points below the highest reading of 13 percent reached in December 2021. Nineteen percent said that labor quality was their top business problem (up 1 point), remaining behind inflation as the number one issue. The frequency of reports of positive profit trends was a net negative 27 percent (seasonally adjusted), 2 points better than March, but still a very poor reading. Among owners reporting lower profits, 33 percent blamed weaker sales, 14 percent blamed the rise in the cost of materials, 13 percent cited usual seasonal change, and 12 percent cited labor costs. For owners reporting higher profits, 43 percent credited sales volumes, 26 percent cited usual seasonal change, and 11 percent cited higher selling prices.

SALES AND INVENTORIES

A net negative 13 percent of all owners (seasonally adjusted) reported higher nominal sales in the past three months, down 3 points from March. The net percent of owners expecting higher real sales volumes rose 6 points to a net negative 12 percent (seasonally adjusted). The net percent of owners reporting inventory gains rose 1 point to a net negative 6 percent. Not seasonally adjusted, 12 percent reported increases in stocks (unchanged) and 17 percent reported reductions (down 5 points). A net negative 4 percent (seasonally adjusted) of owners viewed current inventory stocks as “too low” (e.g. inventories are too large) in April, up 1 point from March. A net negative 6 percent (seasonally adjusted) of owners plan inventory investment in the coming months, up 1 point from March.

COMMENTARY

Although first quarter growth was lower than expected (1.6%), inflation didn’t seem to notice as the inflation rate actually rose a bit to 3.5%, still well out of reach of the 2% goal. The average yearly inflation rate for the 10 years prior to 2021 was 1.7%. The last three years has seen an average yearly inflation rate of 5.8% (2021-2023). This is very important for small business owners. Since 2021, an average of 22% have cited inflation as their top business problem, reaching as high as 37% in July 2022. Only the percent citing labor quality competed for the #1 problem position.

Inflation fell significantly from the 9% reached in 2022 as the economy resolved Covid-related supply chain problems and the government lifted its heavy hand from the economy. But progress beyond 3% levels has hit a wall as firms on Main Street continue to report raising selling prices and labor compensation at historically high levels. An analysis of the factors driving inflation in the small business sector identified compensation gains as the major driver of price increases (along with supply shocks and sales growth).

The percent of firms reporting higher compensation and planning to raise compensation remain historically high, so prices will stay under pressure (unless a recession comes along). The Federal Reserve is trapped by its policies, unable to cut rates when inflation stays persistently high (well over the 2% goal). The decline in the inflation rate from 9% could justify a small policy rate cut, but overall, the Fed needs to see more progress on reducing the inflation rate. Historically, recessions accomplish this, that’s when price cutting becomes more common. Last month’s BLS job report suggests some weakening with only about half as many jobs created compared to the prior months. As things stand now, it is likely that there will be only one rate cut this year (seven were expected last January). Although the interest rate paid on small business loans has doubled from 4% to over 9%, historically low percentages of owners report problems getting the credit they seek.

Overall, owners remain historically very pessimistic, with optimism at low levels and expectations for economic performance in the second half of the year depressed. The election will create more uncertainty about taxes, regulations, and government spending (which has supported growth and job creation for the past two years). Owners will have to deal with a rising level of uncertainty and turmoil, but will continue to do what they do best – serve their customers.

Just knowing NFIB is on your side is cause for optimism

Let’s chat for 10 minutes and we’ll help you understand all the ways NFIB is advocating for you and your business.