- >

- Cost of living>

- Cost of living statistics>

- UK cost of living statistics 2022

UK cost of living statistics 2024

This page includes UK cost of living statistics for 2024, such as changes to average household spending in the UK, the impact of rising inflation on energy bills, council tax, and more.

Statistics surrounding the cost of living in the UK are inescapable. Given that energy bills, food prices and other associated expenditures are already high, and expected to rise further, it’s perhaps not surprising that more and more people are seeking help with the UK cost of living crisis.

Money.co.uk gathered the most recent UK cost of living statistics for 2024, to see how the rising cost of living will impact people, households, and businesses today and in years to come.

Top 10 UK cost of living statistics

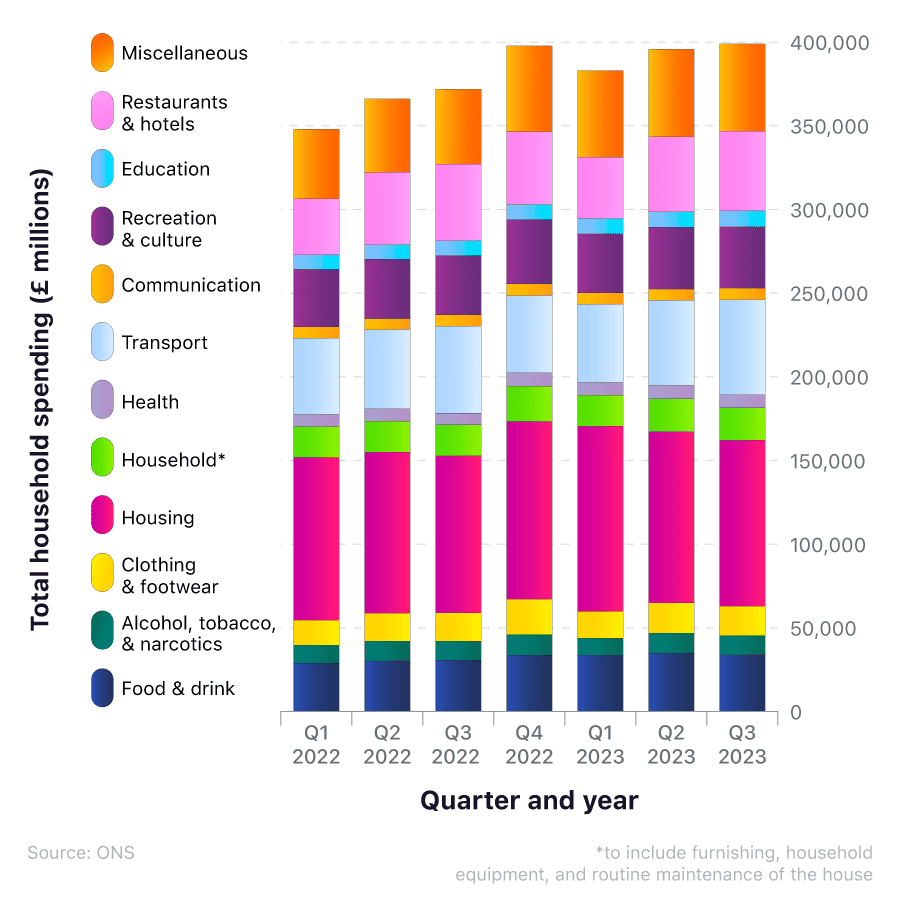

Total household expenditure for the third quarter of 2023 stood at nearly £399 billion

Combined domestic spending for the first three quarters of 2023 was nearly £1.2 trillion

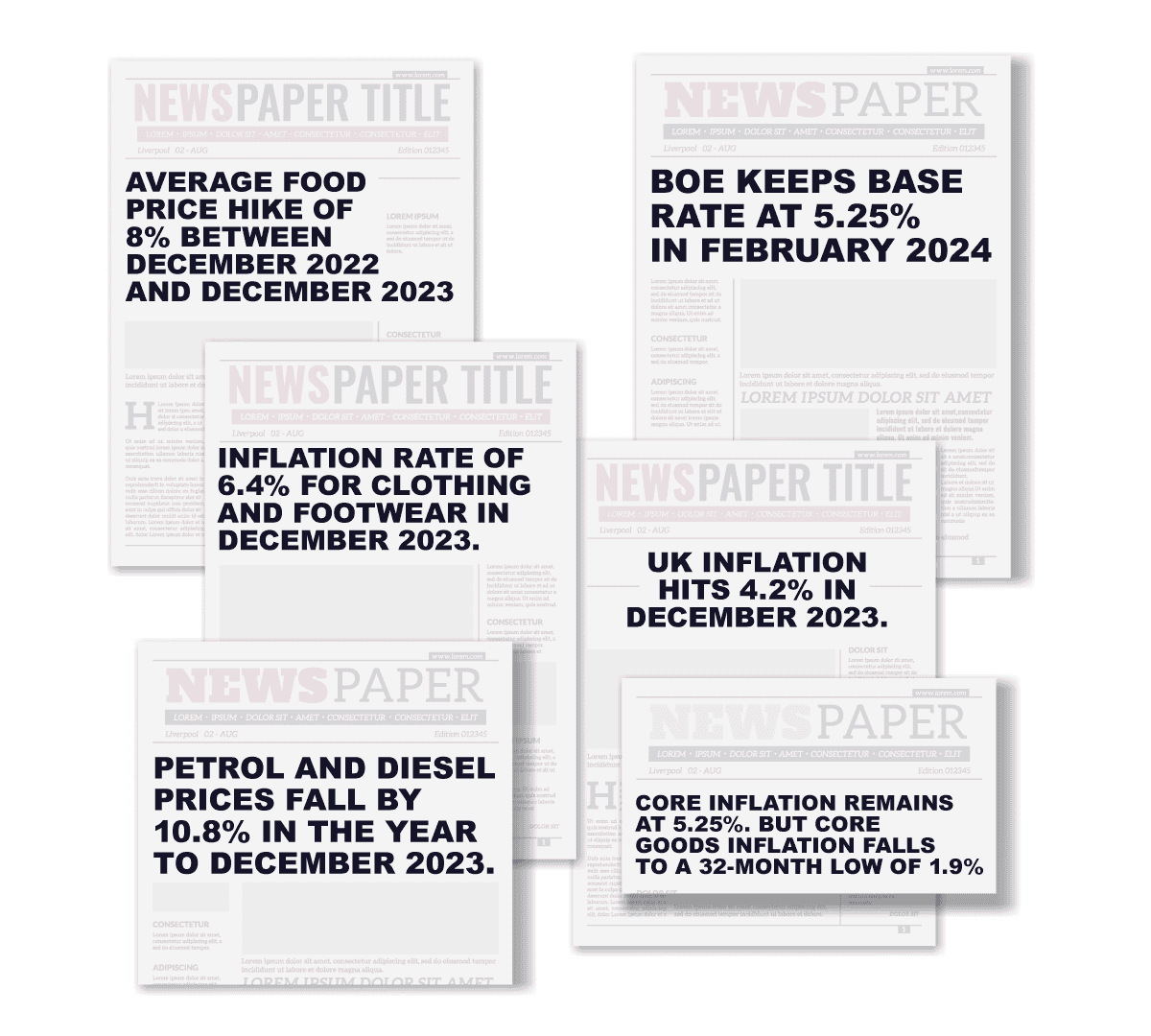

As of February 2024, the BoE base rate sits at 5.25% for the sixth consecutive month

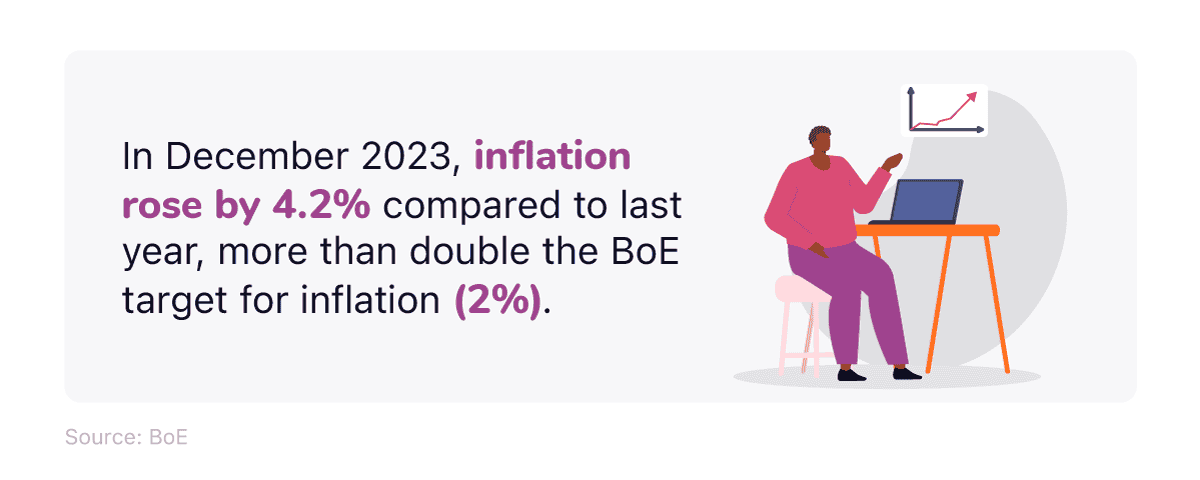

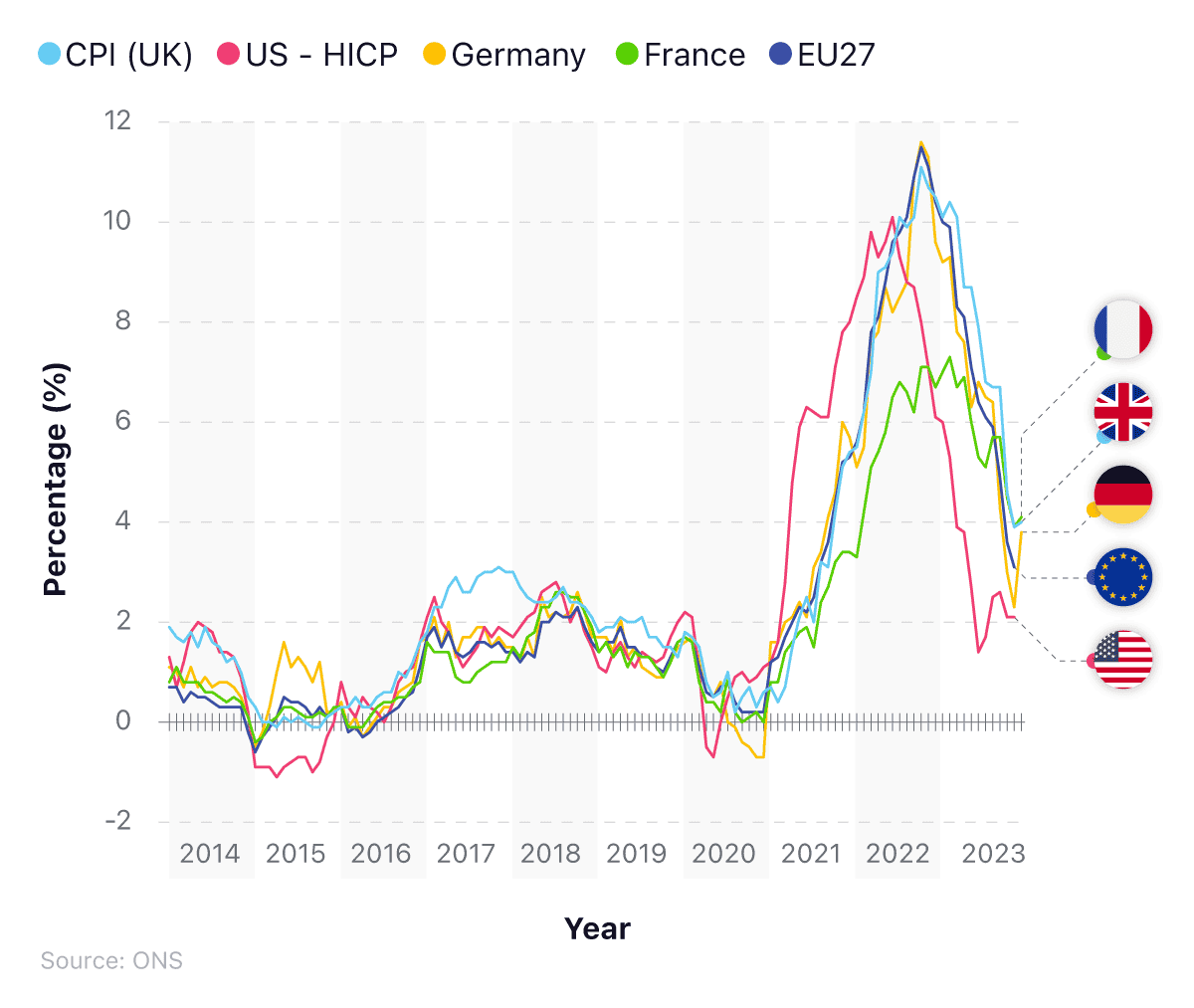

As of December 2023, UK inflation stands at 4.2% – more than double the BoE target of 2%

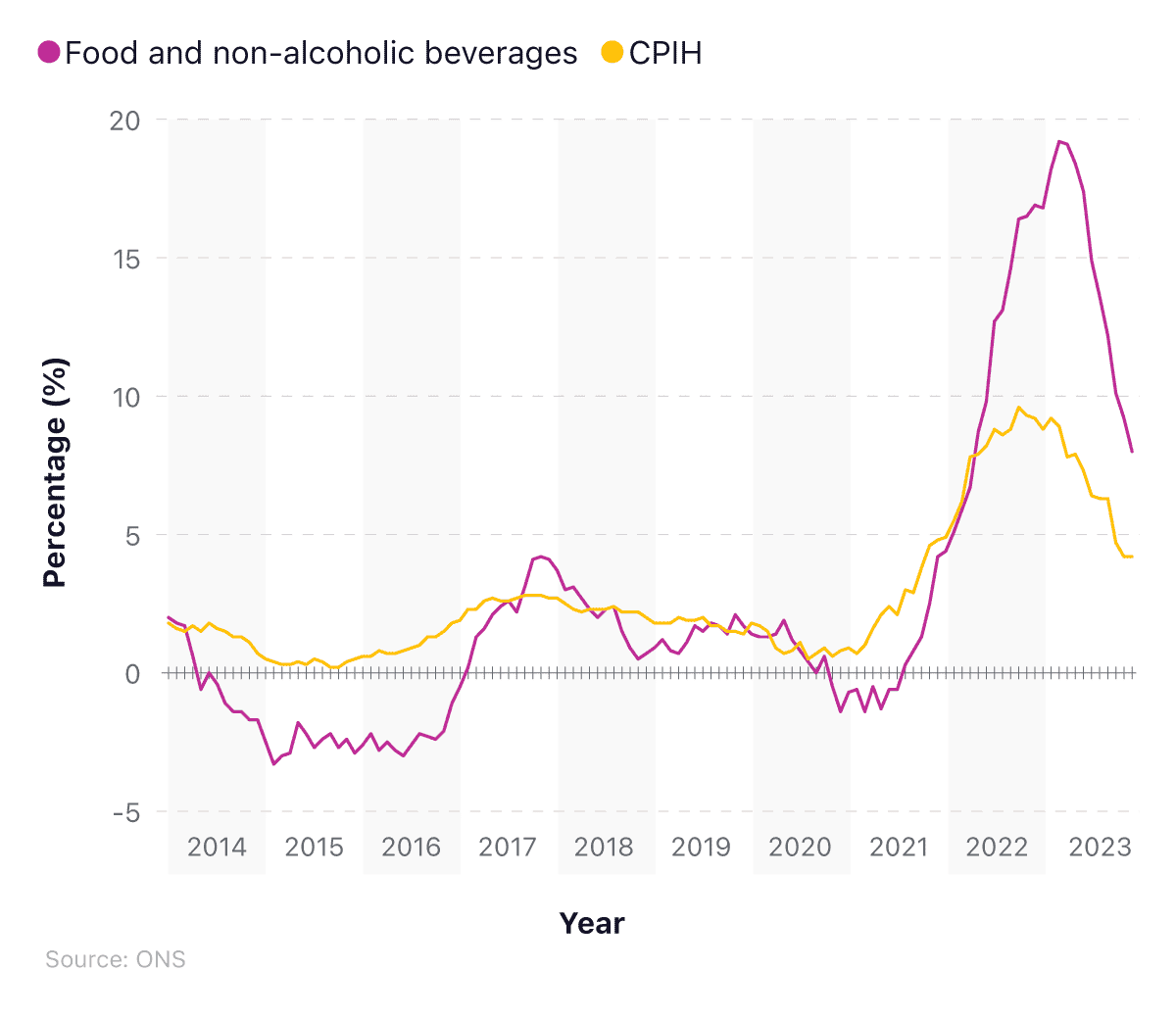

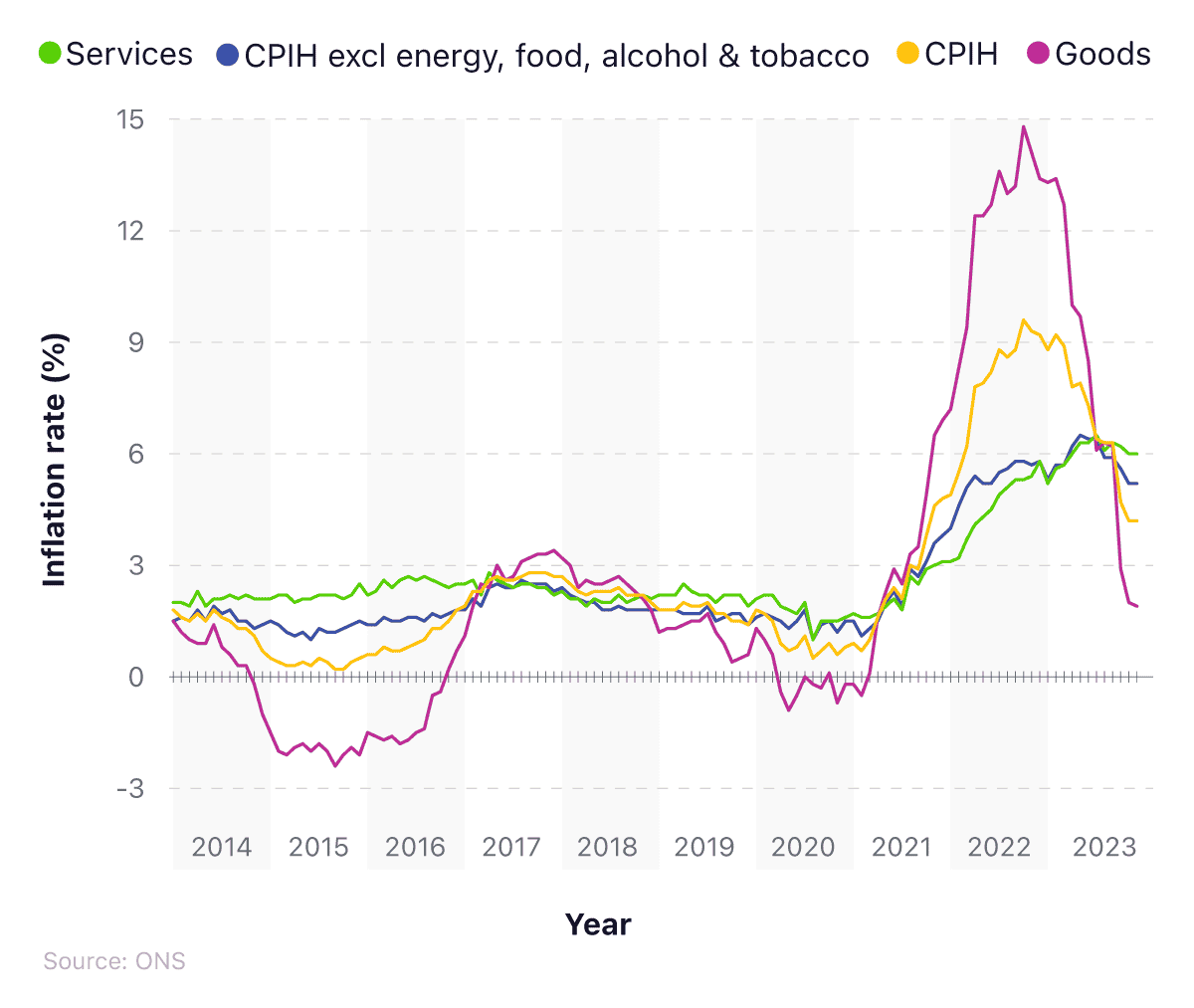

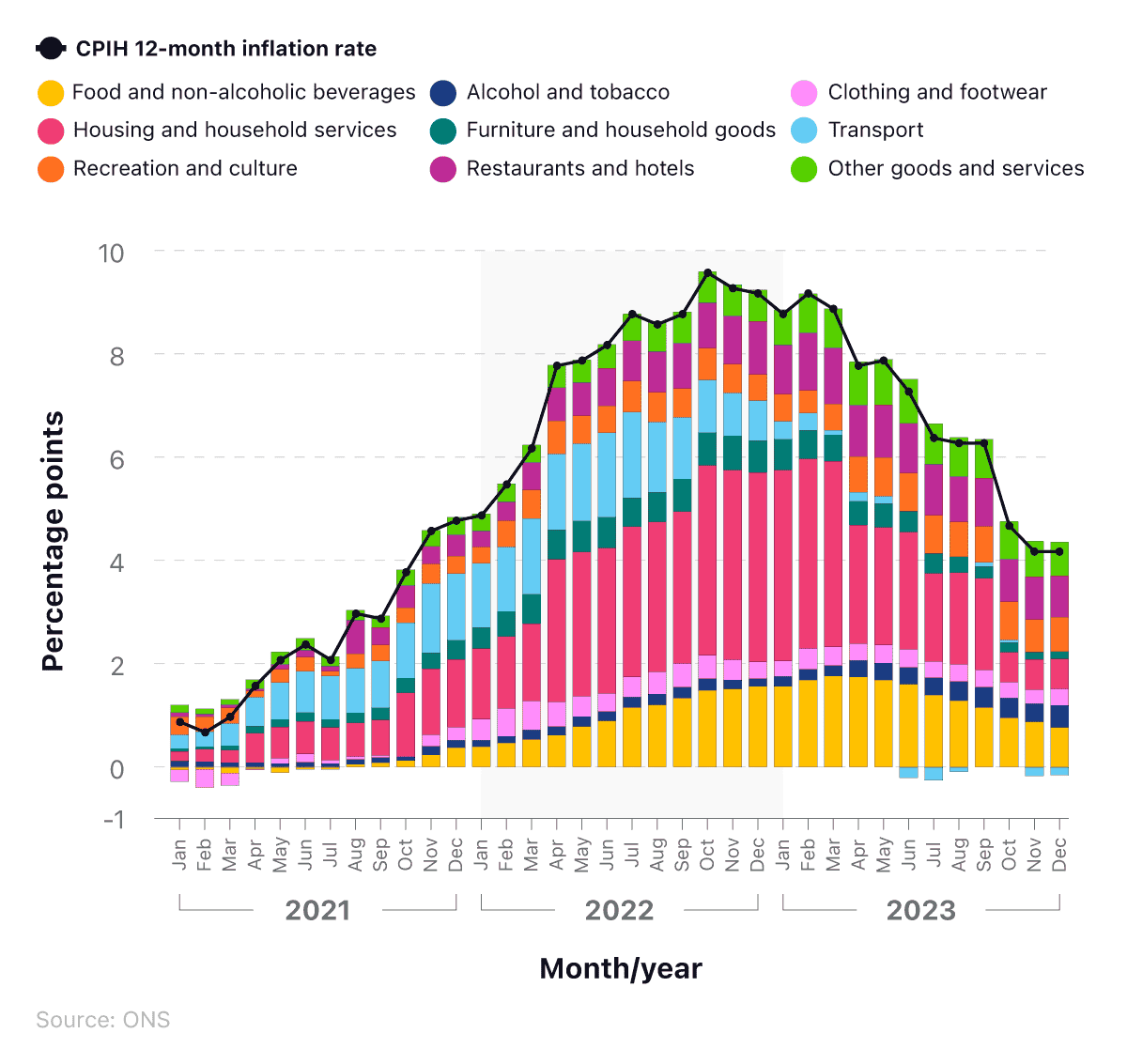

The largest upward contribution to the monthly change in both CPIH and CPI annual rates came from alcohol and tobacco while the largest downward contribution came from food and non-alcoholic beverages.

Total household electricity spending in England and Wales was around £1.3 billion less in 2023 compared to 2022

Annual UK rental price growth stood at +9.7% in December 2023

The average UK adult has approximately £4,123 of unsecured personal debt

According to the Student Money Survey 2022, the average UK living costs for students rose 14% within the previous 12 months, with the average student spending £924 a month

In terms of UK retirement statistics, for a typical UK retiree to have a minimum standard of living once they give up work, they need to be earning at least £12,800 a year

UK household spending statistics

The latest average household spending statistics show that, in December 2023, household spending was up 0.4% from November 2023, and 4.2% compared to December 2022.

A breakdown of total household spending statistics in the UK 2022-23, broken down by category

Total household expenditure for Q3 2023 stood at nearly £399 billion, with around £99 billion spent on housing (25%) and nearly £57 billion on transport (14%).

The data shows a rise in expenditure for every category between Q3 2022 and Q3 2023, with spending on housing increasing by 5.6% over this period.

Total domestic expenditure by UK households

According to UK cost of living stats, total domestic expenditure by UK households was close to £1.5 trillion by the end of 2022 – an increase of more than £160 billion from 2021. Total spending for the first three quarters of 2023 was nearly £1.2 trillion – around £90 billion more than the first three quarters of 2022.

A breakdown of total domestic expenditure by UK households

More than a quarter (27%) of spending in 2022 is attributed to housing, totalling in excess of £393.4 billion. This is followed by nearly £191 billion worth of household spending on transport, and just under £144 billion on recreation and culture. The smallest contributors to the total UK domestic expenditure for 2022 were health (approximately £29.9 billion) and communication (£27.3 billion).

Predicted increase in household expenditure for 2024 (exclusive data)

UK cost of living statistics indicate that those in London are likely to spend almost £411 a month more on living costs in 2024 compared to 2022, whereas residents in the North East are predicted to spend just over £291 a month extra.

However, in terms of percentage increase, the rising cost of household living expenses is expected to be roughly the same across the whole of the UK. All regions are expected to see rises between 18% and 19% in 2024 compared to 2022. The only exception is the South East, which falls just outside this margin (17.98%).

A breakdown of the expected weekly price increase of UK household expenditure in 2024 by region

| 2024 Price Increase (£) | Food & non-alcoholic drinks | Alcoholic drinks, tobacco & narcotics | Clothing & footwear | Housing, fuel & power | Household goods & services | Health | Transport | Communication | Recreation & culture | Education | Restaurants & hotels | Miscellaneous goods & services | Total across all expenditure groups |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| North East | 18.98 | 2.46 | 2.37 | 11.45 | 5.9 | 0.82 | 6.63 | 2.12 | 7.11 | 0.04 | 6.95 | 3.13 | 67.97 |

| North West | 21.2 | 2.91 | 2.98 | 13.69 | 5.85 | 1.06 | 7.76 | 2.39 | 9.57 | 0.28 | 8.5 | 4.39 | 80.57 |

| Yorkshire & The Humber | 19.62 | 2.86 | 2.43 | 11.67 | 6.27 | 1.23 | 7.27 | 2.1 | 8.25 | 0.33 | 7.93 | 4.1 | 74.06 |

| East Midlands | 21.54 | 2.72 | 2.84 | 12.52 | 6.18 | 1.29 | 9.02 | 2.41 | 9.32 | 0.61 | 8.9 | 4.69 | 82.03 |

| West Midlands | 21.64 | 2.65 | 2.94 | 14.04 | 6.15 | 1.49 | 8.18 | 2.41 | 8.72 | 0.42 | 8.17 | 4.45 | 81.28 |

| East | 22.38 | 2.84 | 2.7 | 15.32 | 6.51 | 1.15 | 9.29 | 2.5 | 9.35 | 0.65 | 8.9 | 4.51 | 86.11 |

| London | 24.1 | 2.14 | 3.32 | 25.18 | 5.31 | 1.29 | 7.3 | 2.38 | 8.1 | 1.3 | 10.77 | 4.85 | 96.04 |

| South East | 24.13 | 2.97 | 2.9 | 16.33 | 7.19 | 1.69 | 9.44 | 2.53 | 11.44 | 1.45 | 9.94 | 5.15 | 95.18 |

| South West | 21.98 | 2.97 | 2.77 | 15.07 | 6.3 | 1.29 | 8.59 | 2.4 | 10.33 | 0.7 | 9.25 | 4.54 | 86.19 |

| Wales | 20.56 | 2.74 | 2.56 | 12.13 | 5.81 | 0.93 | 7.02 | 2.22 | 8.38 | 0.48 | 6.83 | 3.77 | 73.43 |

| Scotland | 20.26 | 3.03 | 2.84 | 12.75 | 5.71 | 0.86 | 7.8 | 2.27 | 8.02 | 0.27 | 7.73 | 3.89 | 75.41 |

| Northern Ireland | 24.84 | 3.06 | 3.7 | 10.24 | 6.18 | 1.43 | 7.72 | 2.38 | 7 | 0.33 | 8.75 | 4.39 | 80.02 |

Source: ONS

Those living in London and the South East have seen the biggest monetary increase in their weekly household living costs, at just over £96.04 and £95.18, respectively. Transport costs in the South East have increased by more than £9.40 per week, followed by rises of just under £9.30 a week for the East of England and just over £9 for the East Midlands.

London, the South East, and Northern Ireland have all seen the weekly cost of food and non-alcoholic drinks rise by at least £24. Meanwhile, housing, fuel and power costs in London increased the most, rising by more than £25 a week on average.

If you already have debts, you could consider a 0% Balance Transfer credit card to help reduce your interest payments.

A breakdown of the expected price increases of UK household weekly expenditure by income bracket in 2024

| Income bracket | Food & non-alcoholic drinks | Alcoholic drinks, tobacco & narcotics | Clothing & footwear | Housing, fuel & power | Household goods & services | Health | Transport | Communication | Recreation & culture | Education | Restaurants & hotels | Miscellaneous goods & services | Total across all expenditure groups |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| below £19,200 | 22.28 | 2.14 | 2.9 | 22.28 | 5.1 | 0.9 | 6.07 | 2.4 | 4.72 | N/A | 5.63 | 3.68 | 78.12 |

| £19,200 - £31,400 | 21.57 | 1.85 | 2.48 | 18.18 | 4.33 | 0.65 | 6.33 | 2.91 | 5.73 | N/A | 5.86 | 3.27 | 73.16 |

| £31,400 - £46,000 | 21.6 | 2.5 | 2.54 | 16.67 | 5.6 | 0.89 | 8.07 | 2.58 | 7.43 | 0.53 | 7.5 | 4.34 | 80.28 |

| £46,000 - £69,000 | 22.28 | 2.57 | 3.46 | 15.8 | 7.11 | 1.15 | 11 | 2.78 | 10.56 | 0.51 | 11.04 | 5.04 | 93.3 |

| Above £69,000 | 25.31 | 3.33 | 4.34 | 19.39 | 8.85 | 2.25 | 15.15 | 2.86 | 14.29 | 1.38 | 16.55 | 6.44 | 120.15 |

Source: ONS

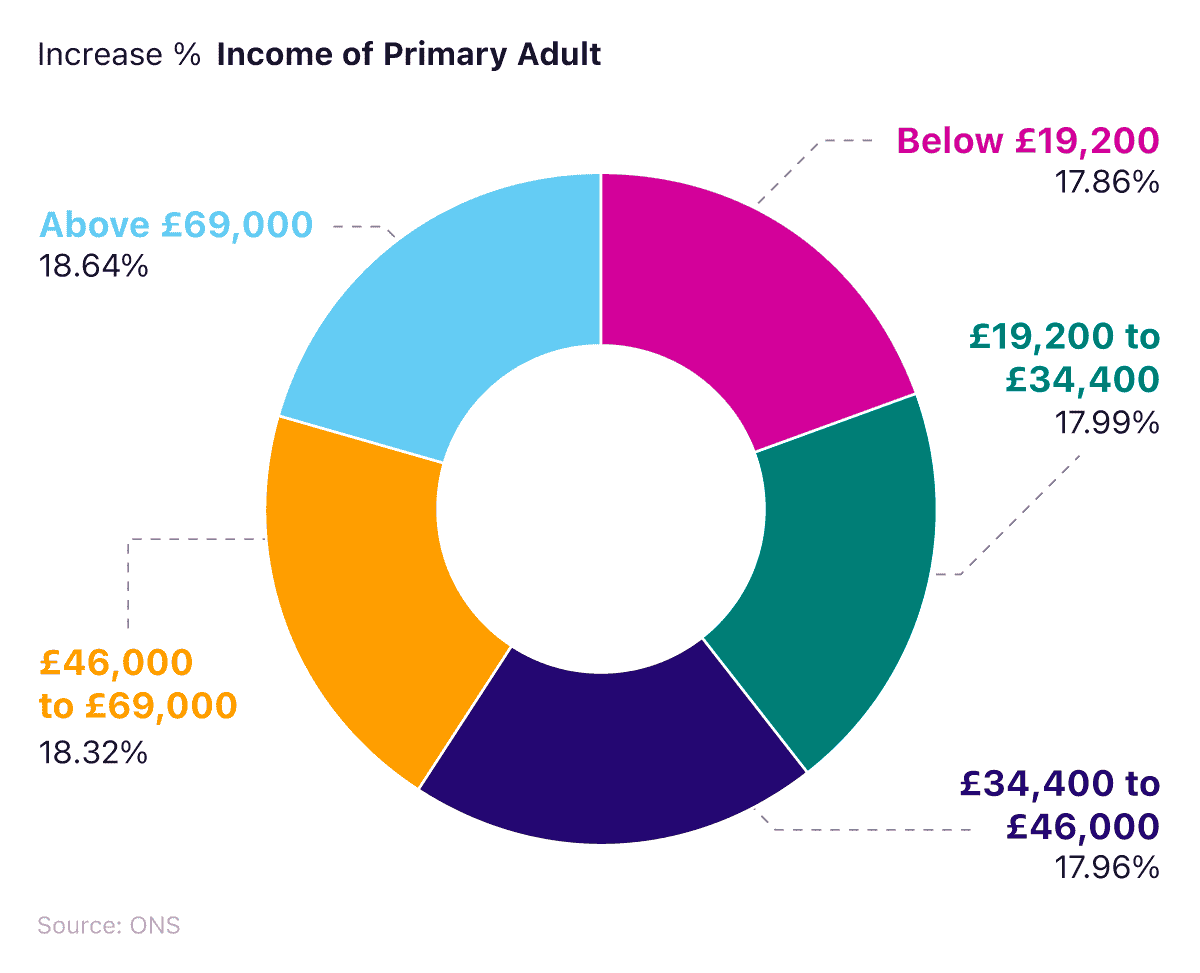

When broken down by income, UK residents earning more than £69,000 a year can expect to see their monthly household expenses increase by around £120 in 2024. Conversely, those earning less than £19,200 a year could see a rise of around £78 a week.

As a percentage increase, all income groups are estimated to see proportionally increased monthly living costs of between 17.9% and 18.6%. Those earning more than £69,000 are predicted to experience increased monthly living costs of just under 18.6% – the highest of all income groups.

According to the UK cost of living stats, those earning between £19,200 and £31,400 a year are expected to have a rise of more than £73 a week in living expenses, with close to £22 a week extra being spent on food and drink and over £18 on housing, fuel and power.

For those earning between £31,400 and £46,000 a year, the biggest proportional change in their weekly spending is also predicted to come from food and housing (just under £22 and £17 extra, respectively.)

This is followed by transport, which may mean paying an extra £8.07 a week for the middle-income earners, and £6.07 a week for those earning £19,200 or less.

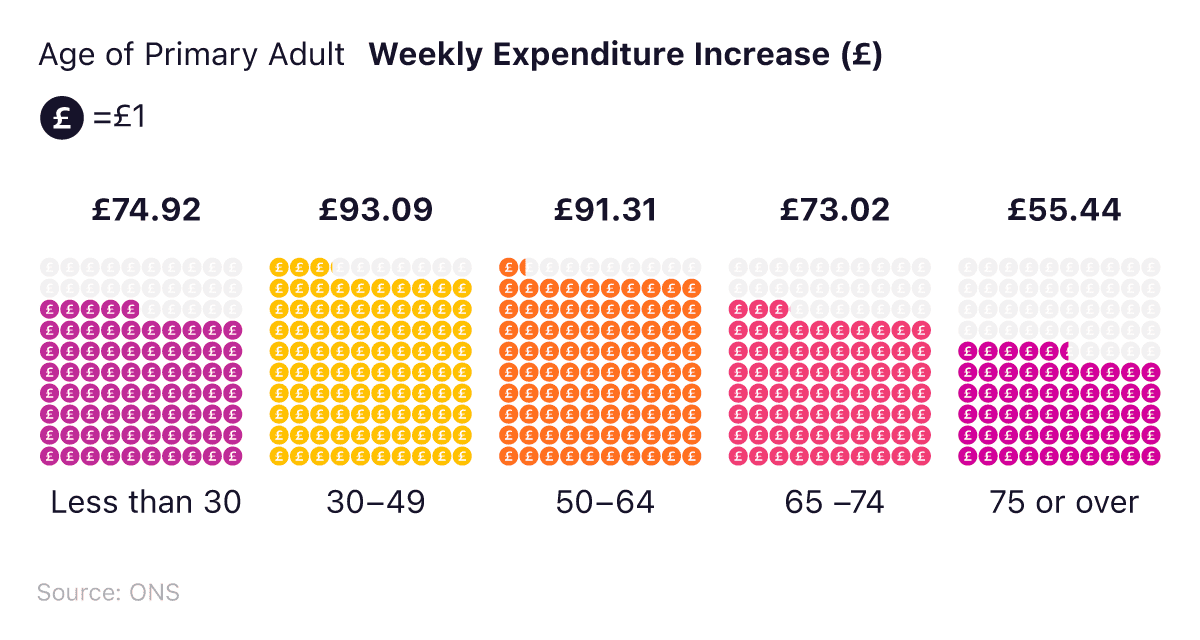

A breakdown of the expected price increases for UK household expenditure in 2024 by age group

| Age of primary adult | Total weekly expenditure up to 2022 (£) | Estimated total weekly expenditure 2024 (£) | Weekly expenditure increase (£) | Monthly expenditure increase (£) | Increase % |

|---|---|---|---|---|---|

| Less than 30 | 419.6 | 494.52 | 74.92 | 321.09 | 17.86 |

| 30 - 49 | 517.5 | 610.59 | 93.09 | 398.96 | 17.99 |

| 50 - 64 | 508.3 | 599.61 | 91.31 | 391.33 | 17.96 |

| 65 - 74 | 398.6 | 471.62 | 73.02 | 312.93 | 18.32 |

| 75 or over | 297.4 | 352.84 | 55.44 | 237.6 | 18.64 |

Source: ONS

When broken down by age, those aged 75 and over could be worst affected by the rising cost of living. The oldest age group could see a rise of 18.64% in their household living costs between 2022 and 2024 whereas, for all other age groups, this could be between 17.9% and 18.3%

UK cost of living stats indicate that, every week in 2024, those aged 30-49 are expected to spend just over £93 more on household costs in 2024 than in 2022. By comparison, those aged 75 and over could see costs rise by over £55 a week.

A breakdown of the expected weekly price increases for UK household expenditure in 2024 by age group and expense category

| Age group | Food & non-alcoholic drinks | Alcoholic drinks, tobacco & narcotics | Clothing & footwear | Housing, fuel & power | Household goods & services | Health | Transport | Communication | Recreation & culture | Education | Restaurants & hotels | Miscellaneous goods & services | Total across all expenditure groups |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Less than 30 | 15 | 1.23 | 1.92 | 24.52 | 4.61 | 0.53 | 6.94 | 2.12 | 5.93 | 0.79 | 7.98 | 3.35 | 74.92 |

| 30 - 49 | 23.53 | 2.31 | 3.49 | 18.91 | 6.16 | 1.18 | 9.57 | 2.65 | 9.41 | 0.95 | 9.77 | 5.16 | 93.09 |

| 50 - 64 | 22.92 | 3.39 | 3.08 | 14.47 | 6.9 | 1.6 | 10.66 | 2.66 | 10.41 | 0.58 | 10.14 | 4.49 | 91.31 |

| 65 - 74 | 19.18 | 3.14 | 2.26 | 10.56 | 6.74 | 1.93 | 6.95 | 2.06 | 8.35 | 0.17 | 7.98 | 3.7 | 73.02 |

| 75 or over | 16.92 | 1.85 | 1.32 | 9.75 | 4.38 | 1.59 | 3.78 | 1.7 | 5.81 | N/A | 4.54 | 3.82 | 55.44 |

(Source: money.co.uk via ONS)

Those between 30 and 64 can expect to witness a rise of between £22 and £24 a week in their food and drink costs, and an increase of between £3 and £4 for clothing and footwear.

Interestingly, the older the age group, the smaller the rise in housing, fuel and power is expected to be. For those under 30 years, housing, fuel and power expenses may increase by an average of £24.52, compared to £9.75 a week for those aged 75 and over.

Looking to cut down on your petrol/diesel expenditure? Check out our guide on how to save money on fuel when driving your vehicle.

Food and non-alcoholic drinks make up another significant area for price increases in 2024, with increases ranging from as low as £15 for the under 30s to as high as £23.53 for those aged 30-49.

High inflation and rising interest rates - consumer goods and food prices

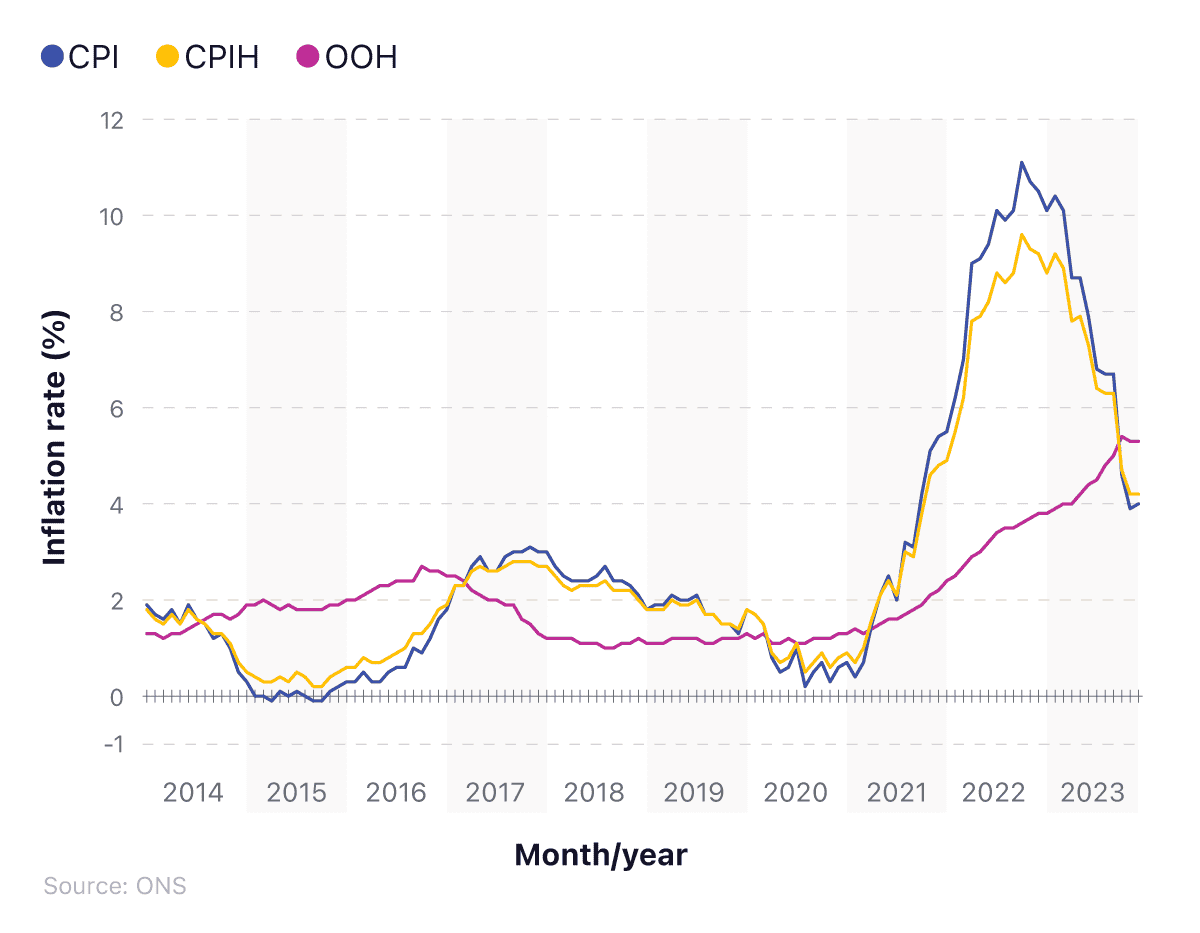

Since 2021, the UK's cost of living has steadily increased. Consumer prices, as measured by the Consumer Prices Index (CPI), were 4.2% higher in December 2023 than the previous year.

On the lips of many are questions about the cost of living—how will it impact them now and in the future? And which areas of life will be affected the most? Let’s start with food.

The price rises for food have accelerated, with the ONS estimating food price inflation to be at 8% as of December 2023. This figure marked the 29th consecutive month in which food prices have risen. These rises are lower than in early 2023, however, when food inflation reached 19.2% in March 2023 – the highest rate since 1977.

A breakdown of UK food price rises by food type between September 2021 and September 2022

| Item | Size (units) | Price in September 2021 (nearest pence) | Price in September 2022 (nearest pence) | September 2021 and September 2022 price change (%) |

|---|---|---|---|---|

| Vegetable oil | 1,000ml | 156 | 258 | 65.20% |

| Pasta | 500g | 38 | 61 | 59.90% |

| Tea | 125g | 67 | 97 | 46% |

| Chips | 1,500g | 99 | 137 | 38.70% |

| Bread | 800g | 48 | 66 | 37.60% |

| Biscuits | 400g | 40 | 54 | 34.40% |

| Mixed frozen vegetables | 1,000g | 76 | 100 | 31.90% |

| Milk | 4 pints | 117 | 152 | 29.40% |

| Crisps | 150g | 73 | 91 | 23.70% |

| Tomatoes | 250g | 48 | 57 | 19.30% |

| Instant coffee | 100g | 131 | 155 | 18.80% |

| Onions | 1,000g | 63 | 75 | 18% |

| Sausages | 454g | 89 | 105 | 18.30% |

| Apples | 6 pack | 83 | 97 | 17.20% |

| Baked beans | 400g | 30 | 34 | 16.20% |

| Potato | 2,500g | 94 | 106 | 13.20% |

| Fish Fingers | 250g | 76 | 87 | 13.10% |

| Tomato ketchup | 460g | 58 | 65 | 12.10% |

| Breakfast cereal | 500g | 69 | 76 | 10.60% |

| Cheese | 255g | 89 | 98 | 10.40% |

| Chicken breast | 600g | 330 | 363 | 10.10% |

| Ham | 200g | 160 | 176 | 9.90% |

| Bananas | 5 pack | 73 | 78 | 7% |

| Yoghurt | 500g | 55 | 58 | 6.60% |

| Fruit squash | 750ml | 48 | 51 | 6.70% |

| Pizza | 300g | 84 | 87 | 3.20% |

| Granulated sugar | 1,000g | 66 | 66 | 0.30% |

| Rice | 1,000g | 89 | 89 | -0.20% |

| Beef mince | 500g | 210 | 195 | -7.40% |

| Fruit juice orange | 1,000ml | 83 | 76 | -8.90% |

Source: ONS

Food budgets during a cost of living crisis are likely to take a hit, as producers are expected to pass any increase in production costs onto you (the consumer).

According to UK lifestyle cost of living statistics, between September 2021 and September 2022, there was a significant shift in the cost of consumer goods—the vast majority of which have seen prices rise.

In 12 months, the price of a 1 litre bottle of vegetable oil increased by over 65% – the highest increase of any UK food item. In September 2021, this would have set customers back £1.56 on average – by April 2022, this had risen to £2.58.

Pasta and tea saw price hikes of nearly 60% and 46%, respectively. Items which experienced rises of between 20%-40% include frozen vegetables, chips, bread, and milk.

Some items saw very little change in their costs, with rice and granulated sugar both experiencing price changes of less than 1%.

Of the 30 items monitored in the ONS survey, just three items decreased in value over the 12 months between September 2021 and September 2022. Orange fruit juice saw the greatest decline, falling by nearly 9%, followed by beef mince (-7.4%) and rice (-0.2%).

The continued rise in the food inflation rate since September 2022 suggests that the majority of items on the table would have incurred further price rises over the last year.

Ways to cut the cost of your weekly shop during the UK cost of living crisis

According to our weekly shop index, the UK ranked as the 22nd most expensive country in the world for food shopping in 2022, with the average food cost per week just shy of £14 per person. By contrast, the same food shop would have set you back more than £20 in the USA (seventh place), and almost £36 in Switzerland (first place).

At the other end of the scale, the same basket of food would have cost you just £6.66 in Turkey and £7.22 in Colombia—roughly half of what it did in the UK.

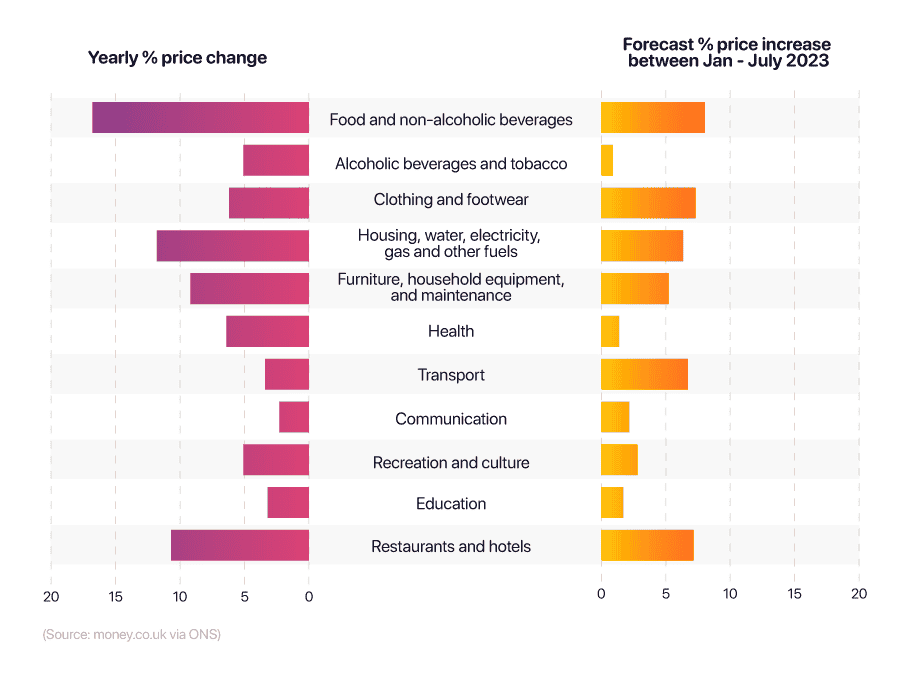

Predicted price changes to UK items 2023 (exclusive data)

To assess the extent of price changes to UK items in 2023, our exclusive study analysed ONS inflation statistics to calculate the percentage price increase for a range of UK products and services between January 2022-23. Using this data, a forecast was generated for potential price rises up until July 2023.

A breakdown of predicted price increases for different categories of household expenditure in 2023

| Item | Yearly % price change | Forecast % price increase between Jan - July 2023 |

|---|---|---|

| Food and non-alcoholic beverages | 16.8 | 8.04 |

| Alcoholic beverages and tobacco | 5.1 | 0.89 |

| Clothing and footwear | 6.2 | 7.32 |

| Housing, water, electricity, gas and other fuels | 11.8 | 6.34 |

| Furniture, household equipment, and maintenance | 9.2 | 5.22 |

| Health | 6.4 | 1.38 |

| Transport | 3.4 | 6.72 |

| Communication | 2.3 | 2.17 |

| Recreation and culture | 5.1 | 2.82 |

| Education | 3.2 | 1.71 |

| Restaurants and hotels | 10.7 | 7.16 |

(Source: money.co.uk via ONS)

According to household expenditure statistics obtained from our exclusive study, all categories of spending were predicted to see a price rise between January and July 2023.

Food and non-alcoholic beverages were expected to see the biggest price rise, costing more than 8% more in July 2023 compared to January. This was followed by restaurant and hotel-related items (+7.16%), such as bed linen, soaps, and cleaning products.

Throughout 2022, food and non-alcoholic beverages saw the largest percentage price increase of all categories (+16.8%) followed by housing, water, electricity, gas and other fuels (+11.8%). However, the predicted future growth for the latter category was expected to be slightly less than that of transport (+6.34% and +6.72%, respectively) going into July 2023.

At the other end of the scale, alcoholic beverages and tobacco were predicted to experience minimal growth in their price, costing just 0.89% more in July 2023 compared to the start of the year. This was followed by health (+1.38%) and education (1.71%).

In terms of yearly percentage price change in 2022, communications had the smallest growth (2.3%), and this was forecast to remain low up until July 2023 (2.17%), although not as low as health or education costs.

A breakdown of highest predicted price increases for different items in 2023

| Item | Yearly % price change | Forecast % price change between Jan - July 2023 |

|---|---|---|

| Passenger transport by air | 18.5 | 59.39 |

| Natural gas and town gas | 132.86 | 35.69 |

| Gas | 129.35 | 35.24 |

| Electricity | 66.71 | 25.24 |

| Liquid fuels | 40.19 | 23.28 |

| Milk, low fat | 45.19 | 19.86 |

| Toll facilities and parking meters | 14.02 | 18.73 |

| Edible offal | 31.49 | 17.95 |

| Milk, whole | 37.14 | 17.27 |

| Diesel | 15.51 | 17.27 |

| Butter | 27.15 | 16.95 |

(Source: money.co.uk via ONS)

In terms of individual items, passenger transport by air was forecast to have the largest percentage price change in the first seven months of 2023, costing almost 60% more in July 2023 compared to six months earlier.

This was followed by natural and town gas and standard gas prices (both around +35%), electricity (+25.24%), and liquid fuels (+23.28%).

Between 2022 and 2023, gas prices saw extraordinary growth, an increase of somewhere between 129% and 133% in January 2023 compared to 12 months earlier. This was almost double the annual price hike rate experienced by electricity costs in the same period, and three times the recorded increase for liquid fuels and low-fat milk.

A breakdown of lowest predicted price increases for different items in 2023

| Item | Yearly % price change | Forecast % price change between Jan - July 2023 |

|---|---|---|

| Equipment for camping and open-air recreation | -1.13 | -7.29 |

| Software | -2.71 | -6.66 |

| Games and hobbies | 1.37 | -6.65 |

| Equipment for the reception, recording, and reproduction of sound and vision | -8.96 | -5.56 |

| Second-hand cars | -7.14 | -4.51 |

| Data processing equipment | -5.14 | -3.66 |

| Personal computers | -7.58 | -3.46 |

| Major items for games and sport | -6.48 | -2.29 |

| Binding services and e-book downloads | 34.32 | -2.29 |

| Coffee machines, tea makers, and similar appliances | -4.6 | -1.9 |

(Source: money.co.uk via ONS)

Throughout 2022, some items experienced a reduction in their price, with equipment for reception, recording, and reproduction of sound and vision seeing the largest drop in cost (almost -9%). The price of second-hand cars and personal computers both saw a decrease in excess of 7% in 2022, followed by major items for games and sports (-6.48%).

Heading into 2023, equipment for camping and open-air recreation was expected to cost almost 7.3% less in July compared to January. Games and hobbies, along with software, prices were also predicted to drop by around 6.6% in the same period.

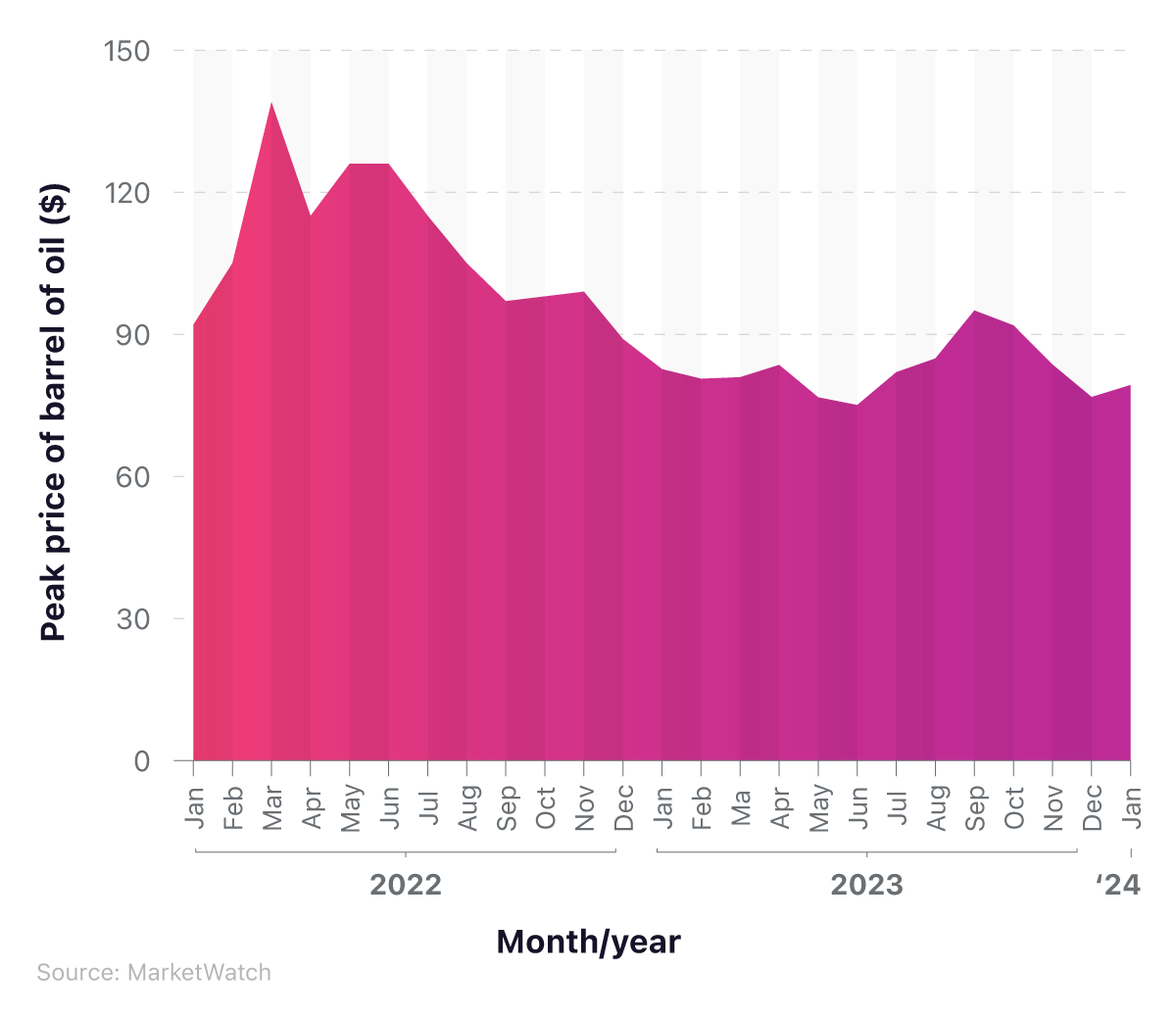

High inflation and rising interest rates - oil prices

The latest UK cost of living crisis statistics show a sharp rise in oil prices between January and February 2022, when the war in Ukraine began. The peak oil price for February 2022 ($100.54) was recorded on 24 February – the day the war was officially announced.

A breakdown of oil prices per barrel in 2023-24

Oil prices peaked at $120.67 in June 2022, amid uncertainty surrounding the war, before falling in the subsequent months. By September 2022, the cost of oil began to approach pre-February 2022 levels (almost $97 per barrel) before declining steadily towards the start of 2023.

Prices fell as low as $67.51 in June 2023 before climbing to $95.03 by late September. Things decreased again toward the end of the year, dropping to $76.76 at the start of December.

As of January 2024, peak oil prices stood at £79.29 – around $9 lower than they were the month before Russia invaded Ukraine. The current state of the world economy may have been a factor in these patterns, with oil prices typically plummeting at times of recession and economic hardship due to a decrease in demand.

Read our guide for tips on saving money on fuel during the cost of living.

UK energy bill statistics

The running costs and energy bills for flats are generally lower compared to houses, especially newly built rented properties with higher efficiency ratings.

UK cost of living statistics indicate that the amount of gas it takes to heat and run a purpose-built flat over 12 months is 40% lower than a converted flat. A one-bedroom home requires less than 50% of the gas needed to heat a three-bedroom house, while D and E energy rated properties require 25% and 48% more gas, respectively, compared to a C-rated home.

Average cost of UK energy bills

The Consumer Price Index (CPI) for all domestic fuels decreased by 2.8% in Q3 2023, compared to Q3 2022. Average domestic energy bills for 2023 were estimated to be £2,592, a 13% (£298) increase on the previous year. The average UK electricity bill was also predicted to increase by 9% to £1,264 over this period, with gas bills incurring a 17% rise from £1,134 to £1,328.

An estimated 557,000 electricity customers and 310,000 gas customers transferred between providers during Q3 2022, representing quarter-on-quarter increases of 41% and 35%, respectively.

Prices in the manufacturing industry for electricity and gas have begun to decrease. The average price (excluding Climate Change Levy) for electricity between July and September 2023 was 18.8 pence per kWh, a 4.7% fall from Q3 2022. At the same time, gas was 4.6 pence per kWh – a decrease of 7.5% over the same period.

Road fuel prices in mid-December 2023 remained lower than at the end of 2022. The mid-month average retail price of unleaded petrol in December 2023 was 142.31p per litre. This was 2.2% lower than in mid-December 2022, when the average cost of unleaded stood at £145.61, and just over quarter (26%) lower than the peak prices at the start of July 2022.

The average retail diesel price was 150.19p per litre in mid-December 2023 – a 15% decrease from the same period a year before and a quarter (25%) drop from mid-July 2022.

Average UK electricity bill costs

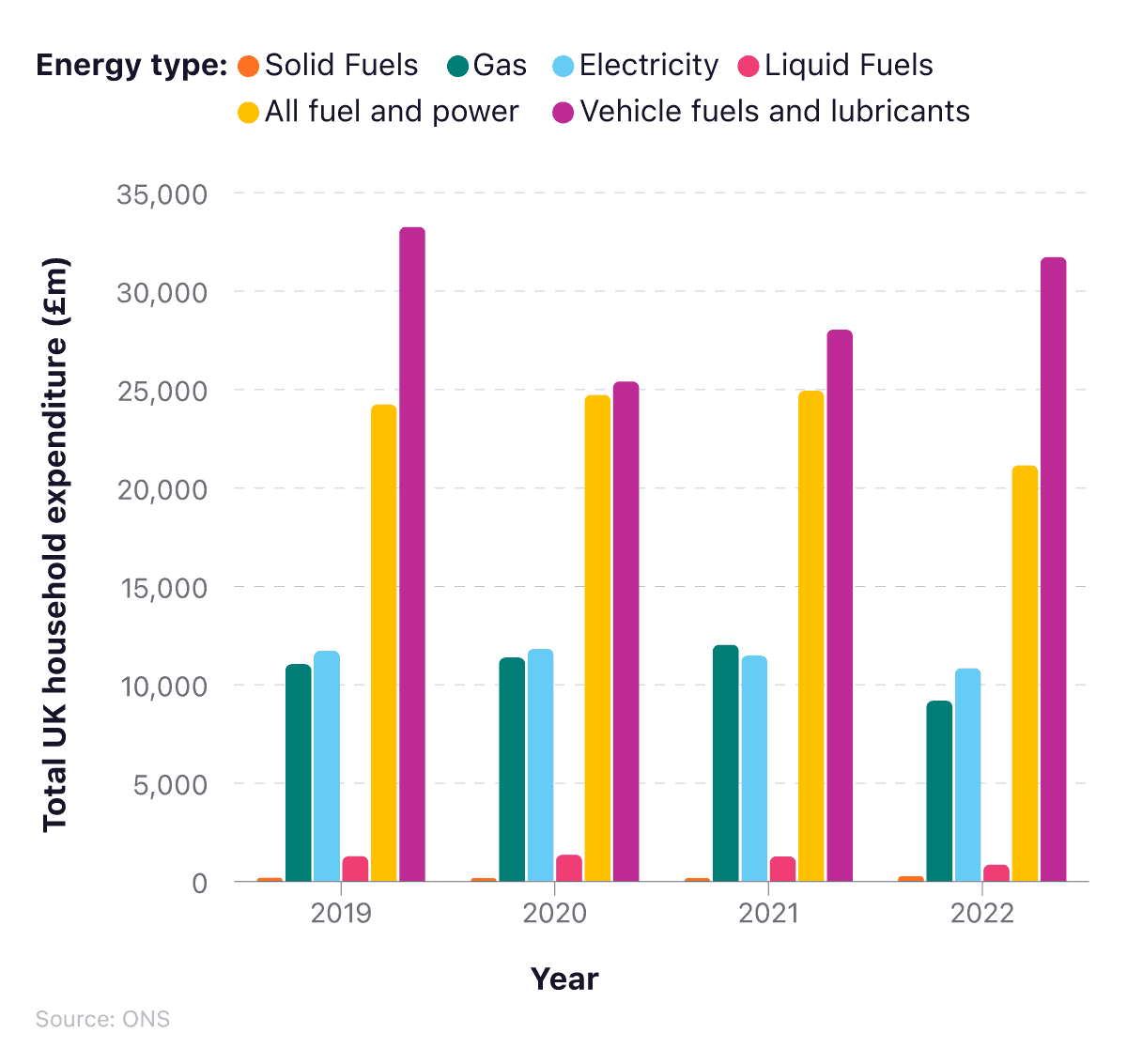

According to UK cost of living stats, energy spending has decreased year-on-year (YoY) since 2019, from almost £55.3 billion, to just under £52.9 billion in 2022. Gas spending fell by more than 14% between 2021 and 2022, from £10.7 billion to just under £9.2 billion.

A breakdown of the total expenditure for different types of energy by UK households from 2020-2022

Electricity spending fell in 2022 by about £1.3 billion (-11%) compared to 2021, while vehicle fuels and lubricants increased to around £31.7 billion — nearly £4 billion more than in 2021.

Average cost of UK electricity bills

The latest statistics on the average cost of UK electricity bills found that, in 2023, the average electricity bill was expected to be £1,264. This represents a rise of around 9% (£104) from 2022. Those on standard credit were paying around 4.5% more than direct debit customers and prepayment consumers.

A breakdown of the average cost of UK electricity bills by year (2021-23)

| Year | Standard credit: All consumers (pounds) | Direct debit: All consumers (pounds) | Prepayment: All consumers (pounds) | Overall: UK (pounds) |

|---|---|---|---|---|

| 2021 | 821 | 754 | 779 | 769 |

| 2022 | 1,226 | 1,151 | 1,122 | 1,160 |

| 2023 | 1,311 | 1,254 | 1,255 | 1,264 |

Source: ONS

All three methods of payment rose hugely between 2021 and 2023, with standard credit consumers increasing by around three-fifths (60%), compared to around two-thirds (66%) for those paying by direct debit and slightly less (64%) for those on prepayment plans.

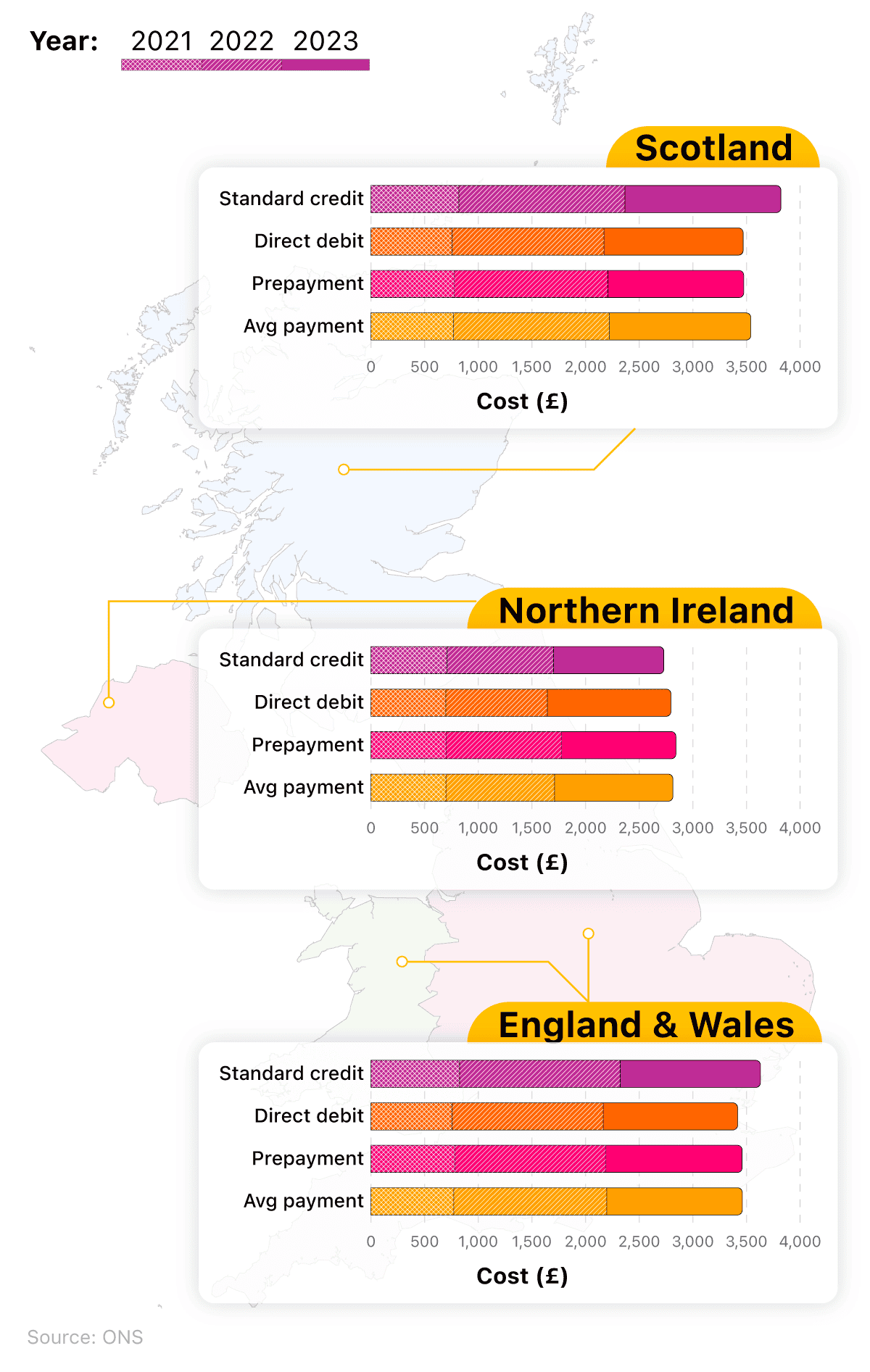

A breakdown of average annual domestic electricity bills between different countries of the UK

The latest cost of living stats on the average electricity bill shows significant price drops across Great Britain. Households in England and Wales paid around 11% less on average on their electricity bills in 2023 compared with the previous year, with those in Scotland paying roughly 9% less.

In contrast, average electricity bills in Northern Ireland increased by 9% from £1,012 a year to £1,103, between 2022 and 2023.

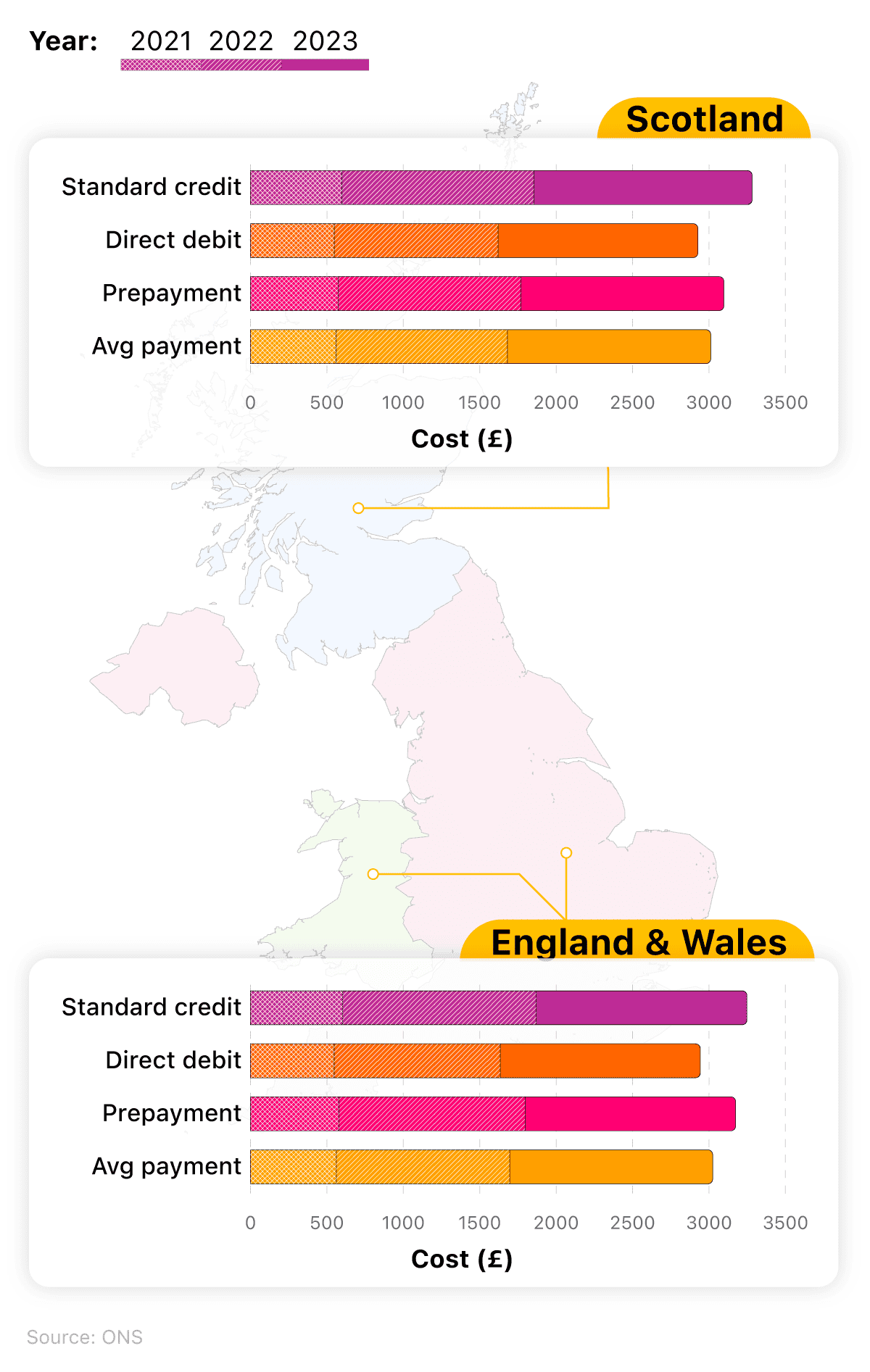

The most expensive method of payment in Scotland in 2023 was by standard credit (£1,454 a year). This is around two-fifths (42%) more costly than paying by the same method in Northern Ireland.

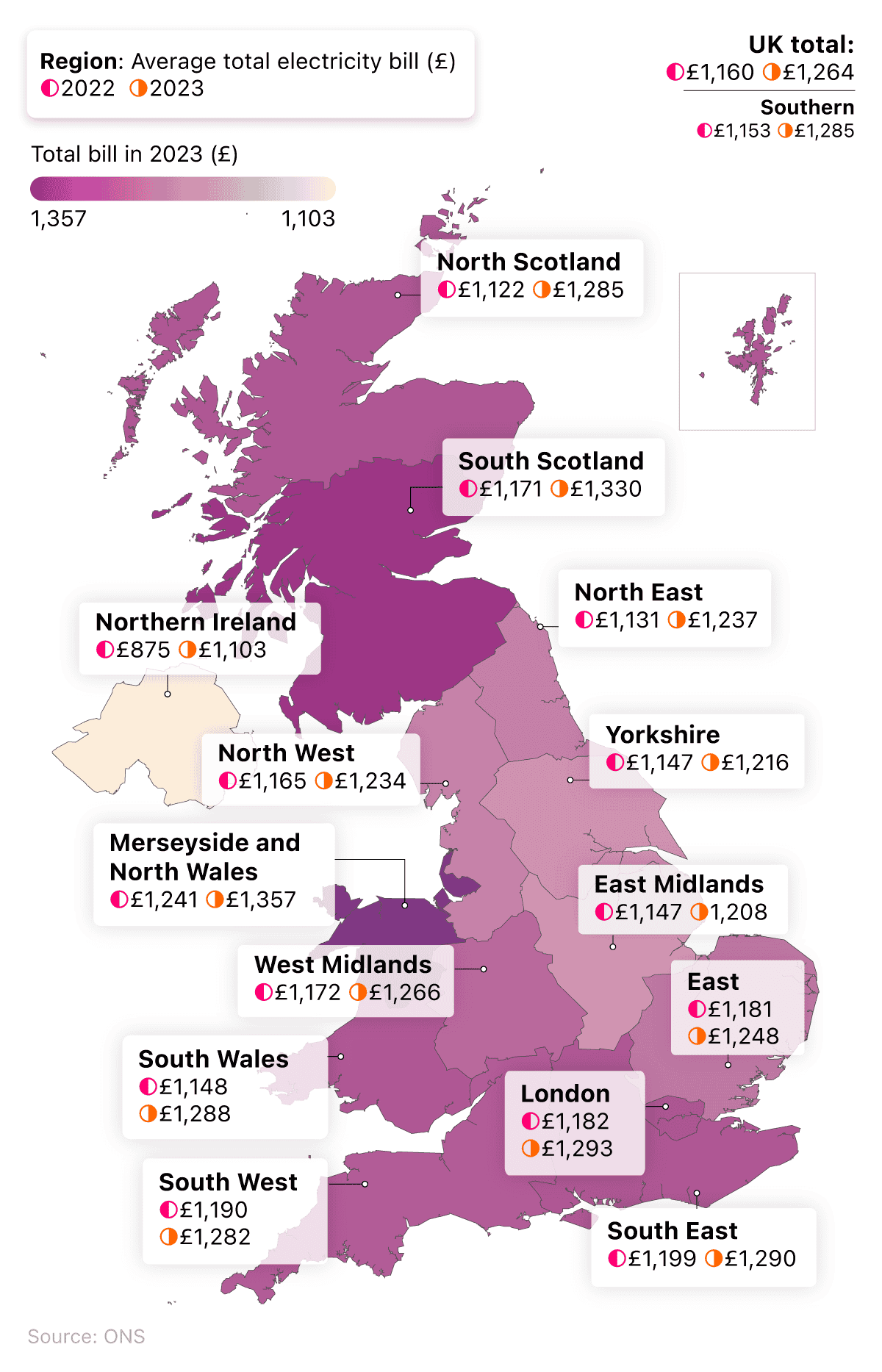

A breakdown of average annual domestic electricity bills between different regions of the UK

Latest UK cost of living statistics show that all regions of the UK experienced rises in their total domestic energy bills between 2022 and 2023. For the UK as a whole, households spent an average of £1,264 on their electricity costs in 2023 – nearly 9% more than the previous year.

In 2023, the highest average UK electricity bills were for those residents in Merseyside and North Wales (£1,357 a year), followed by South Scotland (£1,330) and London (£1,293). By contrast, the cheapest annual electric bills could be found in Northern Ireland (£1,103), followed by the East Midlands (£1,208) and Yorkshire (£1,216).

South Scotland had the most expensive unit cost for standard credit payments at 41.25p/kWh. This is 12.73p/kWh more than Northern Ireland – the cheapest location per unit.

Northern Ireland also had the cheapest bills for prepayment customers, with their average annual fees (£1,063) costing around £290 less than those in the West Midlands (£1,353) – the most expensive region for this payment method.

Average electricity bills for direct debit customers are cheapest in Yorkshire and the Humber with average annual fees of £1,152 – £201 less than Merseyside and Wales.

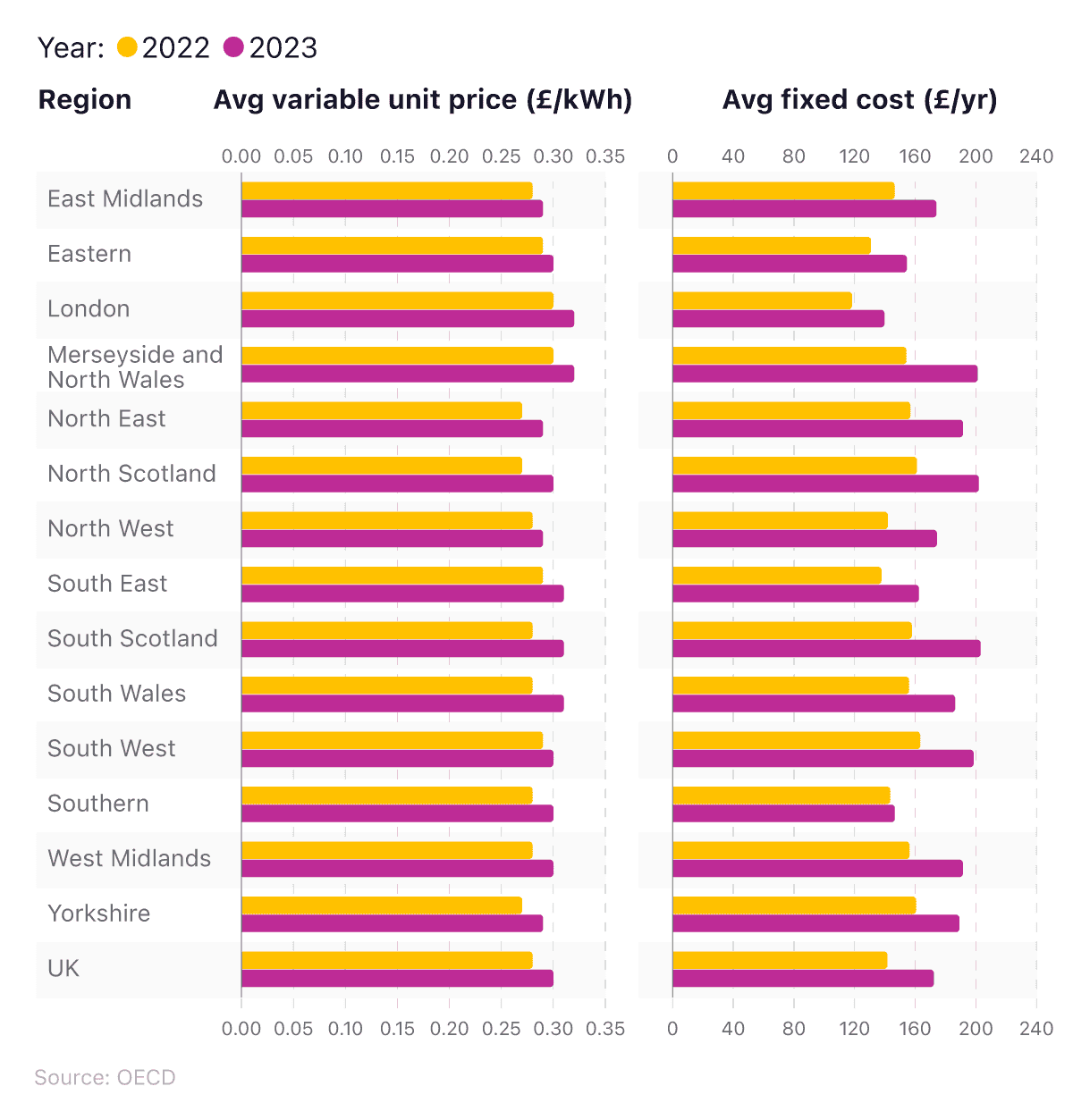

A breakdown of average units costs and fixed costs for electricity across different regions

In 2023, UK households spent, on average, in excess of £172 a year on fixed-cost electricity bills. This represents a rise of around a fifth (22%) from 2022.

Those living in North Scotland typically incur the costliest annual electricity bills for fixed charges, at over £203 a year. This is around 45% more expensive than London (£139.63).

The average variable rate for those paying by standard credit, direct debit, and prepayment methods fell somewhere between £0.28/kWh and £0.35p/Kwh for all regions. South Scotland proved to be the costliest region for standard credit payments and direct debits, with the West Midlands being the most expensive for prepayment plans.

At the other end of the table, Londoners typically paid the lowest costs for all three payment plans, with their average direct debit fixed cost of £132.43, around £67 lower than the average costs in the most expensive region, South Scotland.

Average UK gas bill costs

After large rises between 2021 and 2022, UK households generally experienced smaller increases in their gas bills for 2023. According to UK cost of living statistics, the average UK gas bill for domestic use was £1,328 in 2023. This was a 17% rise on the average from the previous year.

A breakdown of the annual average UK gas bills 2021-23

| Year | Standard credit: All consumers (£) | Direct debit: All consumers (£) | Prepayment: All consumers (£) | Overall: UK (£) |

|---|---|---|---|---|

| 2021 | 601 | 550 | 587 | 564 |

| 2022 | 1,266 | 1,086 | 1,217 | 1,134 |

| 2023 | 1,381 | 1,308 | 1,372 | 1,328 |

Source: ONS

Standard credit consumers, on average, pay more than direct debit or prepayment customers. In 2023, standard credit payments were found to be £1,381 on average. This was £73 a year more than direct debit customers and £9 a year more than those on prepayment plans.

Learn how to write a budget that will help you stay on top of your finances and manage your money better.

A breakdown of the annual average gas bills for different countries of Great Britain

Across all payment types in England and Wales, the average gas bill for 2023 was £1,328. This was an increase of more than 17% from the previous year. In Scotland, the average cost was £1,330 – up nearly a fifth (19%) from 2022.

Those on standard credit payments in England and Wales pay, on average, £1,377 a year for their gas. This is £69 a year more than those on direct debit in the same countries.

In Scotland, those on standard credit pay just under £1,427 a year for their domestic gas consumption. This is £120 more than those on direct debit and £100 more than prepayment customers.

A breakdown of average annual domestic gas bills for different regions of Great Britain

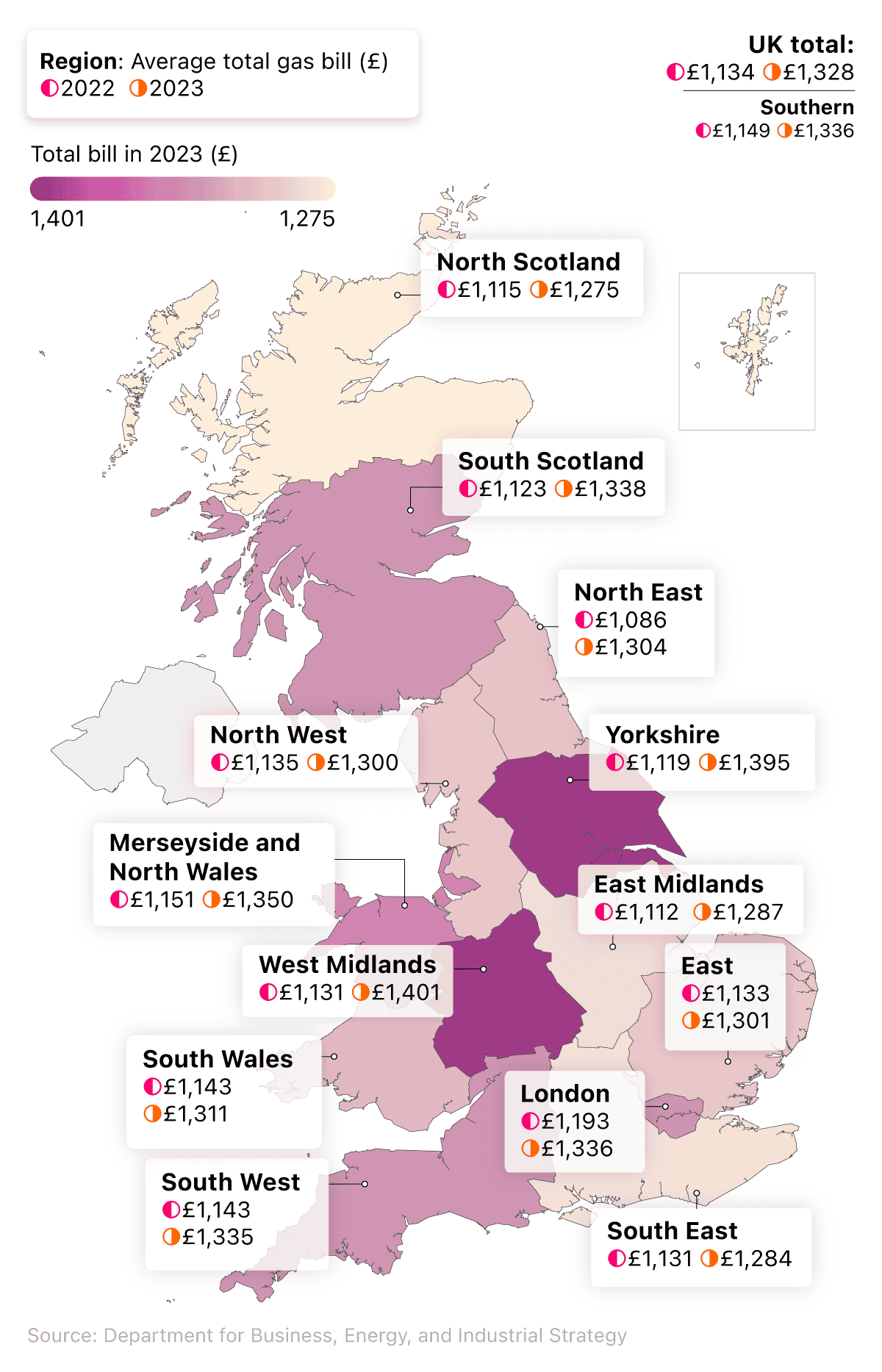

All regions of Great Britain experienced rises in their total domestic gas bills between 2022 and 2023. For the UK as a whole, households spent an average of £1,328 on their gas costs in 2023 – a 17% increase on the previous year.

The highest average gas bills in 2022 were for those living in the West Midlands (£1,401 for the year), followed by Yorkshire (£1,395). By contrast, the cheapest annual gas bills were found in North Scotland (£1,275) and the East Midlands (£1,287).

South Scotland had the most expensive unit cost for standard credit payment in 2023, at 10.57p/kWh (0.77p/kWh more than the North East – the cheapest location per unit). As a result, those living in South Scotland were paying £34 more a year than those in the North East for a standard credit payment.

Customers in the West Midlands face the most expensive bills for direct debit payments (£1,392), typically paying £150 a year more than those in North Scotland by comparison. However, this was the cheapest payment option for the majority of regions within the country.

For prepayment customers, Yorkshire is the most costly area, at £1,481 a year. This is £158 a year more than those in South Scotland, who only pay £1,323 on average for their domestic gas bills.

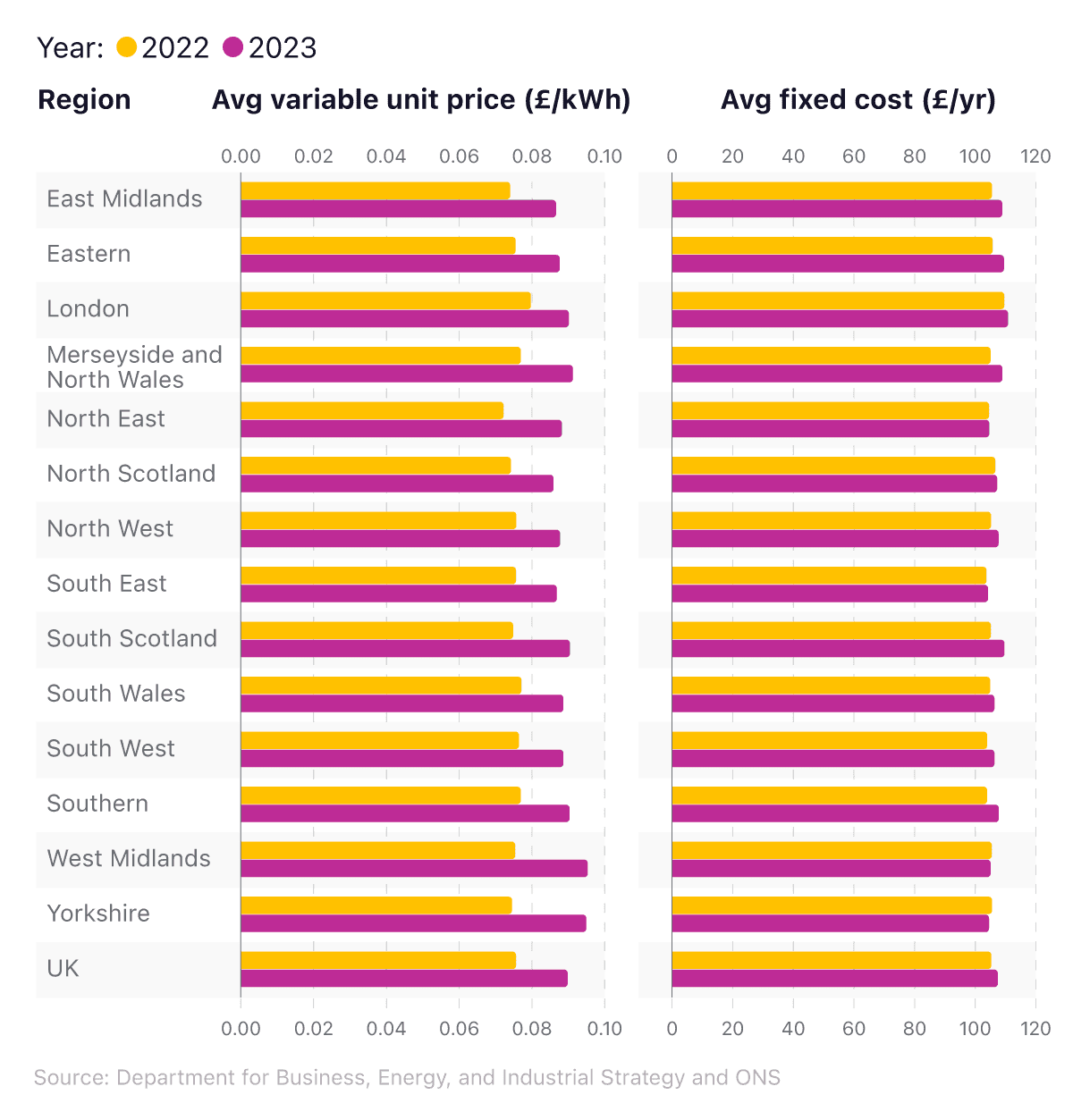

A breakdown of average units costs and fixed costs for gas across different UK regions

In 2023, British households spent, on average, £107.41 a year on fixed costs on their gas bills. This represents a rise of just over 2% from 2022.

Those living in London incurred the costliest fixed charges in 2023, at just over £110.79. This is more than £6 a year higher than the cheapest part of Great Britain (the South East).

Those in London also paid the most on standard credit and prepayment plans with rates close to £122.02 and £123.55, respectively. Those on standard credit in the capital paid more than £5 more than those in South East – the cheapest region for standard credit.

South Scotland had the most expensive charges for direct debit customers, with an average cost of £106.84 – more than £5 higher than the cheapest region (the West Midlands).

UK prepaid energy meter statistics

Prepaid energy meters are an increasingly popular type of domestic energy meter that requires users to pay for energy before using it. This ‘pay as you go’ system has become popular amongst low-income households and those looking to save money as it allows the customer to track their usage in real time and reduces the risk of spending more than they can afford for gas and electricity.

In some instances, energy providers can switch customers to prepaid meters if they have missed payments or have an outstanding debt for energy bills. Based on figures from Ofgem, an estimated 600,000 people were forced onto a prepayment meter in 2022 because they could not afford their energy bills, a rise of 220,000 from the previous year.

A breakdown of UK households with prepaid energy meters in 2021 (weighted figures)

| Number of households on prepaid energy meters for gas only (millions) | Number of households on prepaid energy meters for electricity only (millions) | Number of households on combined prepaid energy meters for gas and electricity (millions) |

| 1.94 | 2.6 | 0.22 |

(Source: ONS)

The latest prepaid energy meter statistics from the ONS found that, as of 2021, around 2.6 million UK households were using combined prepaid energy meters for their electricity. Electricity-only meters were found to be the most common type of prepaid energy meters amongst UK households.

Figures for gas-only prepaid meters were around 25% less than electricity meters, with just under 2 million households using this variant. Conversely, those who used combined pre-paid meters for gas and electricity only were far less common, with this type of meter found in roughly 90% fewer households than gas-only meters and 92% less than electricity meters.

A breakdown of UK households with prepaid energy meters in 2021 where the referenced household person is unemployed (weighted figures)

| Number of households on prepaid energy meters for gas only (thousands) | Number of households on prepaid energy meters for electricity only (thousands) | Number of households on combined prepaid energy meters for gas and electricity (thousands) |

| 266 | 330 | 9 |

(Source: ONS)

* A Household Reference Person (HRP) is the person who is legally responsible for the household. Where there is more than one person who is legally responsible in the household, the HRP is the person with the highest income. If there is more than one person with the same income, the eldest member of the household becomes the HRP.

The figures regarding the number of unemployed households with prepaid energy meters follow a similar pattern to the overall statistics. Again, the most common type of prepaid meter was found to be electricity-only meters, with this type of meter found in roughly 25% more households than the next most common pre-paid meter (gas only).

Combined meters were once again the least common pre-paid meter, with their figures of 9,000 more than 95% lower than both electricity-only and gas-only meters.

A breakdown of UK households with prepaid energy meters in 2021 receiving disability benefits (weighted figures)

| Number of households on prepaid energy meters for gas only (thousands) | Number of households on prepaid energy meters for electricity only (thousands) | Number of households on combined prepaid energy meters for gas and electricity (thousands) |

|---|---|---|

| 414 | 554 | 36 |

(Source: ONS)

Cost of living stats found that electricity only meters were also the most common type of pre-paid meter amongst those receiving disability benefits. Found in over 550,00 households, this type of meter was found in more than 30% more homes than gas-only meters. In a trend that mimics the previous findings, combined meters were once again found in over 90% fewer homes than both electric and gas pre-paid meters.

UK energy price cap

A price cap is introduced to stop companies from making excessive profits and ensure consumers pay no more than a fair price for their energy consumption. It’s traditionally updated twice a year and tracks the wholesale energy cost to decide how much the cap should be.

After dozens of energy suppliers became insolvent as a result of soaring prices not keeping up with the six-month review process, Ofgem changed this to a quarterly process in August 2022.

Under the UK energy price cap, companies can pass on ‘reasonable costs' to the consumer, including any increases associated with buying gas from its source. From April 2022, energy companies were also allowed to pass this additional cost onto UK customers because they cannot afford to supply gas and electricity for less than they have paid for it.

Between 2021 and 2022, 29 energy companies either left the market or were put into administration due to rising global gas prices. This affected around 4.3 million UK customers.

In February 2022, the UK regulator Ofgem announced the UK energy price cap would increase from 1 April 2022 by 54%, from £1,064 to £1,971 for typical annual consumption.

Following concerns over a mammoth rise in prices just as winter began, the Government stepped in to limit the UK energy price cap to £2,500 for a typical household from October 2022. The Energy Price Guarantee (EPG) meant that the government would subsidise any customer payments above £2,500 between October 2022 and March 2024.

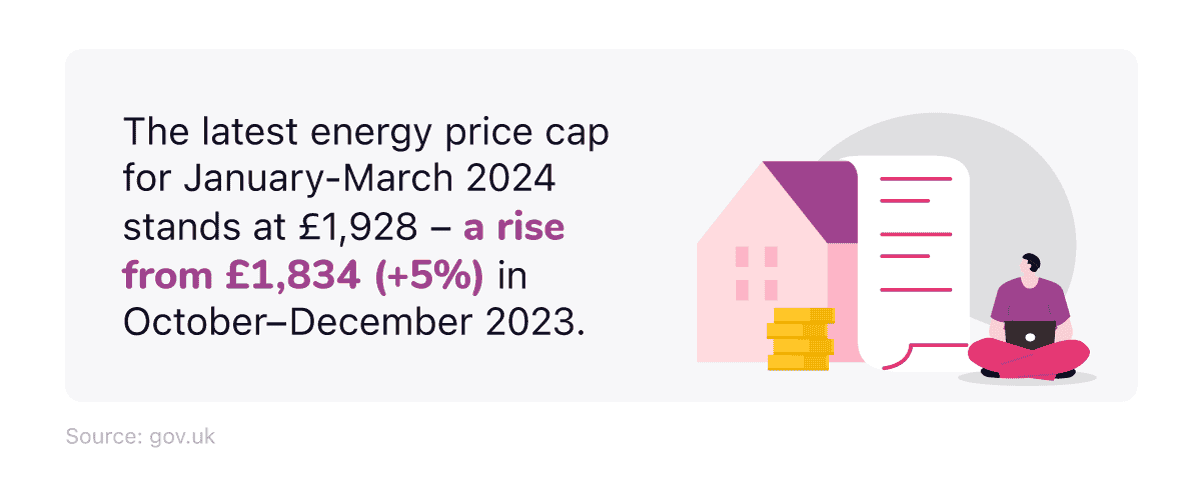

The energy price cap peaked at £4,279 in January 2023, before falling throughout the rest of 2023. The latest energy price cap for January-March 2024 stands at £1,928 – a rise from £1,834 (+5%) from October-December 2023 for those paying by direct debit.

The UK energy price cap is a limit on the cost of a unit of gas/electricity, with standard charges taken into account. It is not a cap on consumers’ overall energy bills, which will rise and fall in line with their overall energy consumption. From 1 January 2024, the equivalent per unit level of the price cap is 28.62p per kWh for electricity and 7.42p per kWh for gas for the average customers paying by direct debit.

The UK energy price cap has directly impacted approximately 29 million UK consumers, particularly those on default or variable rates on credit metres. This could affect customers in various ways, depending on how they choose to pay their energy bills. For example, from January-March 2023:

Those on default tariffs paying by direct debit could see an increase of almost £94, from £1,834 to £1,928 a year

Prepayment customers (about 4.5 million UK households) may experience a rise of £99, from £1,861 to £1,960. This could result in additional fees of £32 a year compared to those on direct debit payment plans

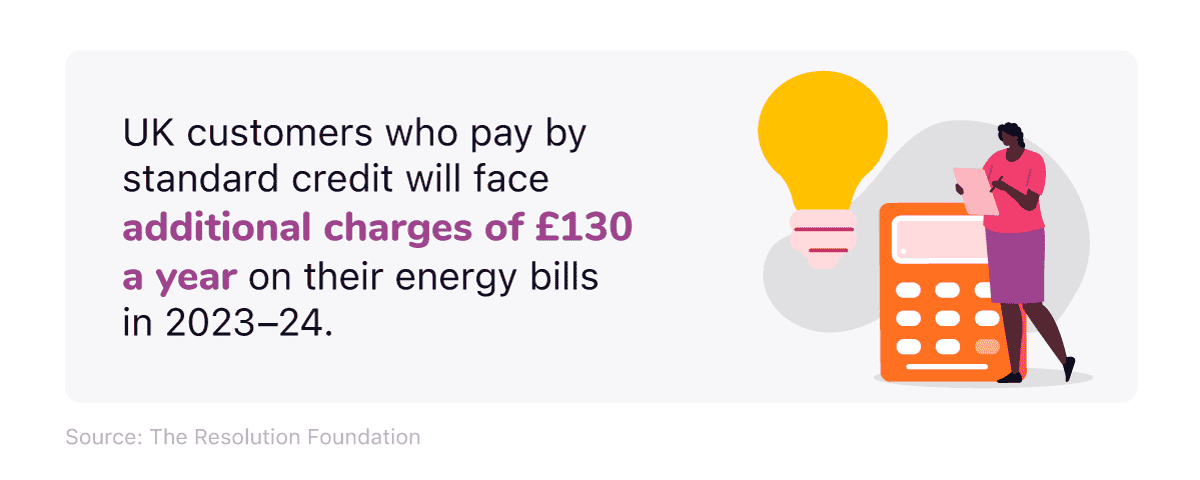

Customers who pay by standard credit (i.e. cash or cheque) could pay an additional £130 more than those paying by direct debit due to the higher admin costs involved in supplying them

The reduction in the UK energy price cap from the start of 2024 is the result of global gas prices falling from their record rates in 2022, with wholesale prices dropping by 86% from their peak in 2022.

Struggling to cover the cost of your energy? Check out our guide on what to do if you cannot pay a bill.

Average UK water bills 2022-23

As of 2023, the cheapest average UK water bill was supplied by Portsmouth Water. With an average of £109 a year, their customers were £28 a year better off than the next cheapest, Bournemouth (£137), and £44 better off per year compared to Cambridge Water in third (£153). By contrast, the most expensive water bill was supplied by Essex and Suffolk, at an average of £245 for 2022 and £225 for 2023 (more than double Portsmouth Water’s average bill).

A breakdown of average UK water bills by company and associated cost (current and forecast) 2022-23

| Company | Average annual cost of bill in 2021-22 (£) | Average annual cost of bill in 2022-23 (£) | Projected average annual cost of bill in 2023-24 (£) |

|---|---|---|---|

| Portsmouth | 103 | 109 | 117 |

| Bournemouth | 143 | 137 | 140 |

| Cambridge | 151 | 153 | 161 |

| South Staffs | 158 | 160 | 173 |

| Northumbrian | 161 | 177 | 188 |

| Southern | 178 | 168 | 186 |

| Hafren Dyfrdwy | 171 | 179 | 195 |

| Affinity (Central) | 177 | 175 | 187 |

| Affinity (Eastern) | 204 | 207 | 227 |

| SES Water | 187 | 190 | 216 |

| Yorkshire | 186 | 186 | 198 |

| Bristol | 189 | 201 | 213 |

| Severn Trust | 188 | 201 | 213 |

| Dwr Cymru Welsh Water | 185 | 193 | 193 |

| Anglian | 195 | 198 | 222 |

| Affinity (South-East) | 232 | 235 | 257 |

| United Utilities | 203 | 199 | 210 |

| Essex and Suffolk | 225 | 245 | 259 |

| Thames | 220 | 227 | 258 |

| South West | 222 | 215 | 216 |

| Wessex | 233 | 235 | 261 |

| UK average | 199 | 199 | 215 |

(Source: Individual companies listed above via Statista, 2023)

*Average bills from April 2023 to March 2024 are estimates based on forecast data provided by water companies)

According to average UK water bill statistics, the projected figures for 2023 and 2024 place Wessex Water as the most expensive water provider in the UK, with an average annual water bill of £261.

Portsmouth is expected to hold onto its crown of the most affordable region for domestic water bills in 2023, with a rise of £6 in its average bill, to £117 a year.

Of the 22 companies, 19 increased their average annual water bills between 2022 and 2023, two decreased them, and only one (Cymru Welsh Water) held them level. South West Water decreased the most (£6 off their average annual bill), while Thames increased the most (£38).

Check out our guide for expert tips that can help you save money on your water bill.

UK housing cost of living statistics - rising house prices

Average UK house prices 2023

Average UK house prices decreased by 2.1% over the year to November 2023, signalling a steeper decline than the 1.3% year-on-year decline seen in October 2023. The average UK house price was £285,000 in November 2023, a £6,000 decrease from the same time in 2022.

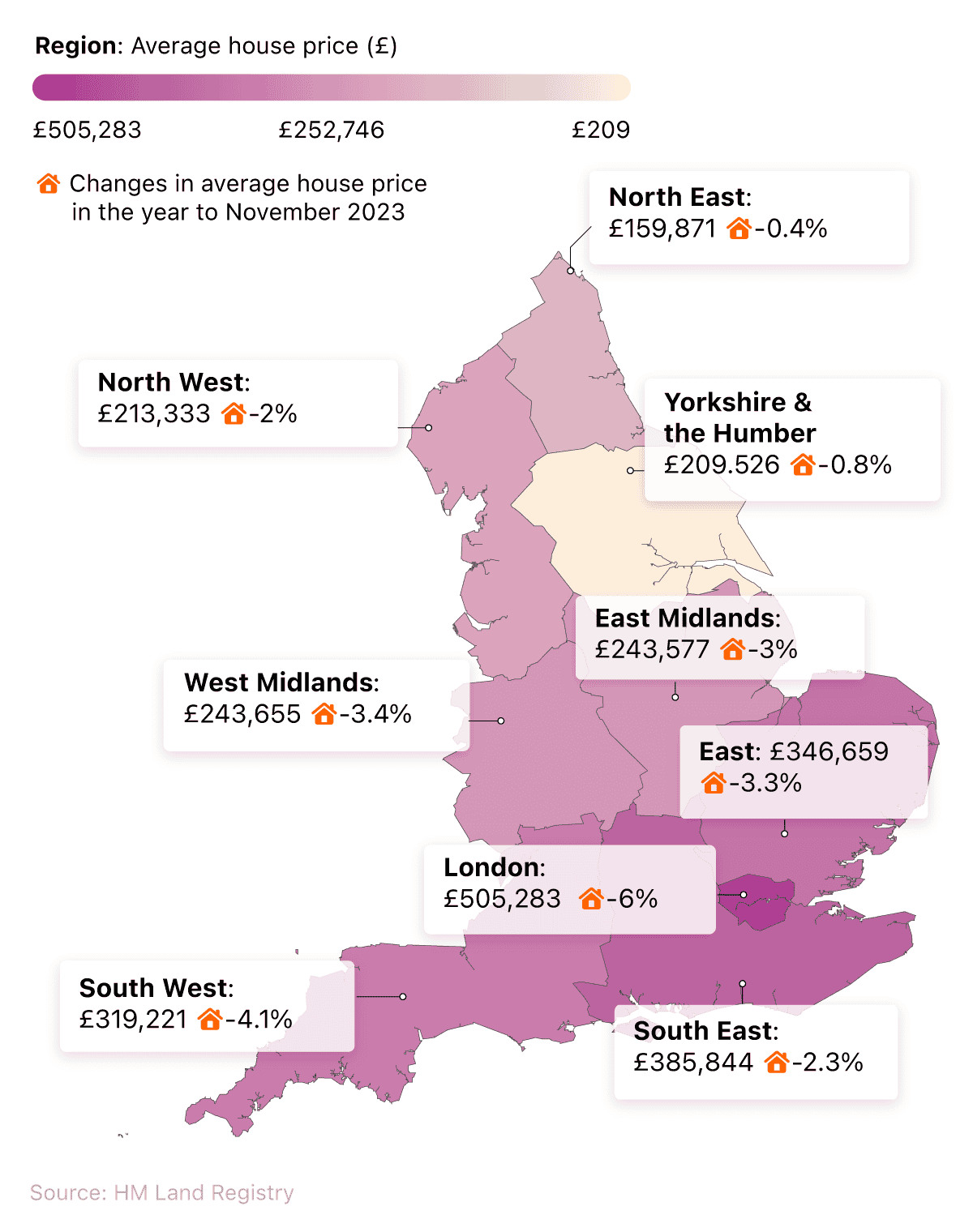

A breakdown of regional average property prices in England 2023

The latest UK cost of living statistics show that London remains the most expensive area to purchase a property, with the average price exceeding £505,000. At the other end of the table, the North East was found to be the most affordable part of England on average for house prices, with prices typically under £160,000 – around two-thirds (68%) lower than London.

The region with the largest fall in average UK house prices since November 2022 was London (-6%), followed closely by the South West (-4.1%). The North East saw the smallest annual price fall, at -0.4%.

As of January 2024, Rightmove reported that the average price of new properties coming to the UK housing market was around £359,748 (a 1.3% rise on the previous month). This suggests that house sellers are continuing to raise their asking prices, despite the fall in average UK house prices. On average, this equated to more than £4,571 per property.

A breakdown of the rate of annual change to average UK house prices between 2019-23

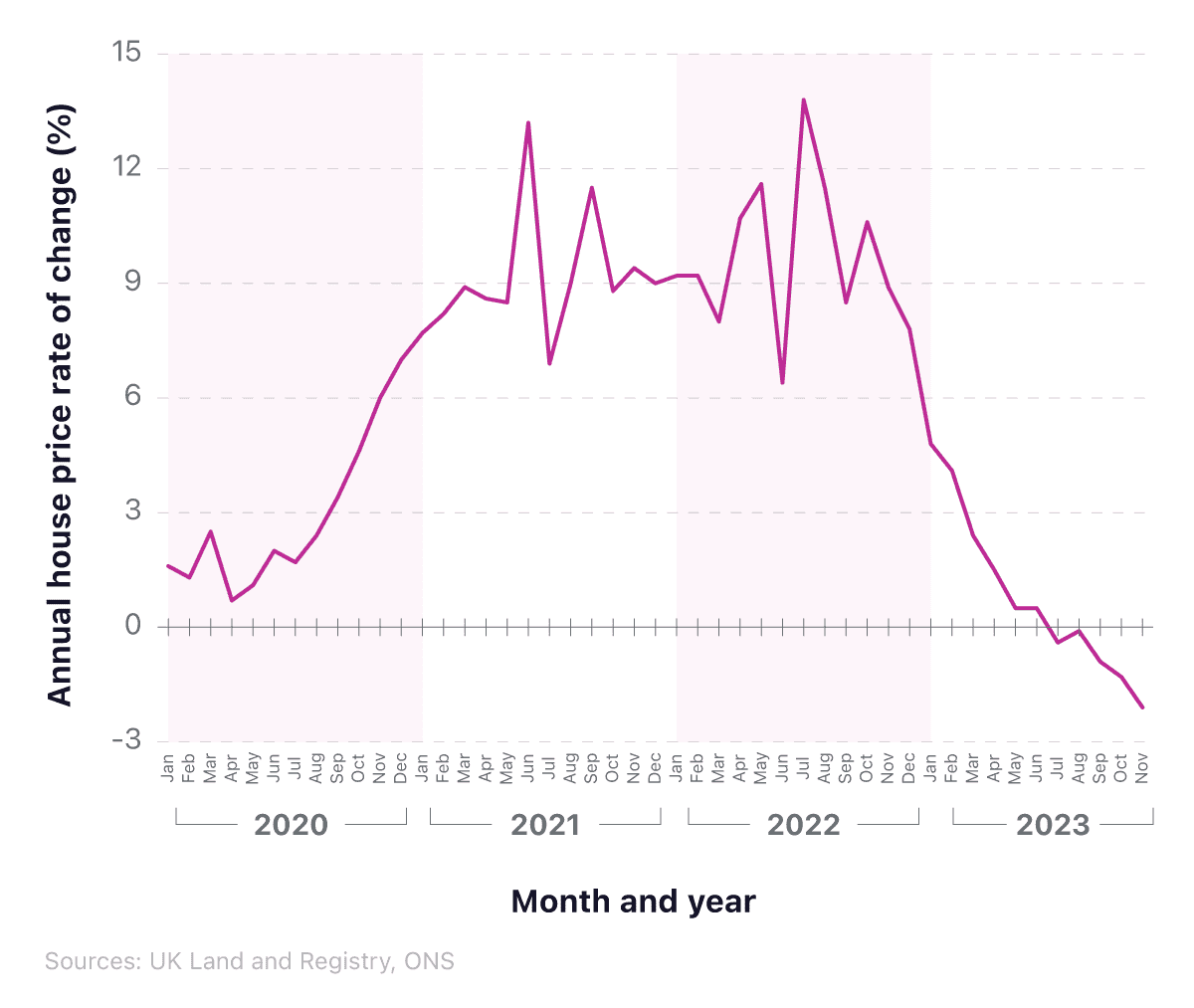

Throughout 2021 and 2022, the UK housing market witnessed a degree of turbulence, with fluctuations between roughly 7-14%. From January 2018, the percentage change dropped from 4.3% to 0.6% in August 2019, after which it rapidly increased to 8.9% in March 2021.

According to UK cost of living crisis statistics, this reached a peak of 13.8% in July 2022 before broadly slipping in the following months. After a 10.6% change in October 2022, the final few months of the year saw a steady decline to 8.9% in November and 7.8% in December.

The percentage rate fell to 4.8% in January 2023 then continued decreasing throughout 2023, dropping below 0% in July (-0.4%) for the first time since 2012.

The latest figure of -2.1% for November 2023 is the lowest figure for house price inflation since June 2011.

Visit our mortgage guides section to find expert advice on new and existing mortgages.

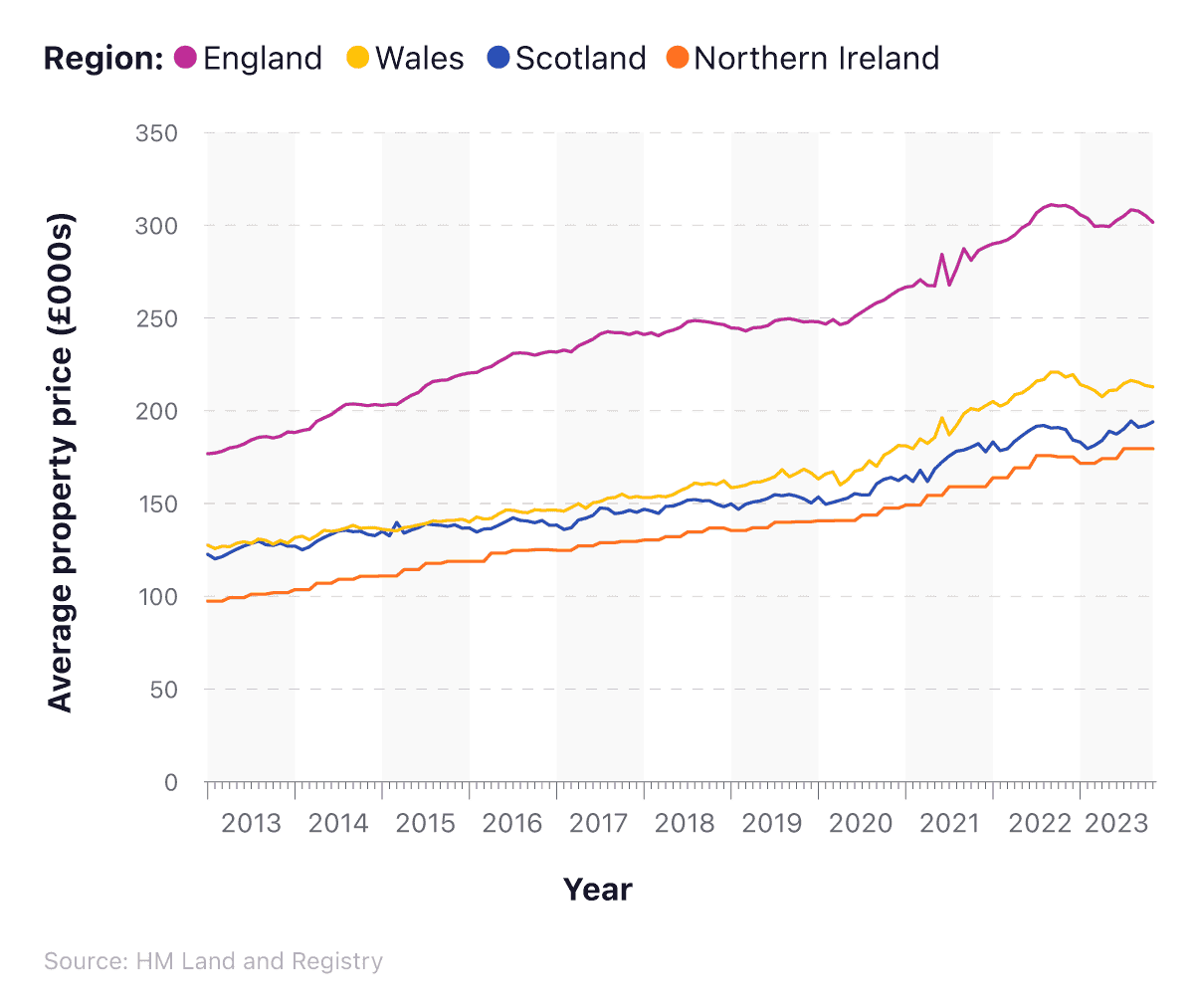

A breakdown of average property prices between different countries of the UK between 2013 and 2022

UK cost of living statistics indicate that the average English property decreased in value in November 2023 to £301,613 (-2.9% compared to November 2022).

In Wales, the corresponding figure was £212,866 (down 2.4%), while Scotland was marginally over £194,000 (+2.2%). Northern Ireland remains the cheapest part of the UK to purchase a property, with average prices of £179,530 in November 2023 (+2.5% from November 2022).

At the start of 2012, the average price of a house in England was just a little more than £174,000 (around 42% less than November 2023). In Wales, the corresponding figure for January 2012 was around £127,000 (40% less than 2023), whereas in Northern Ireland, the average property will set you back around £80,000 more in 2022 compared to 2012.

Scotland has seen the smallest growth in its property prices across the last 10 years. In 2012, the average property would set you back around £123,000 (just £71,000 less than in 2023).

Average UK house prices by property type

According to recent UK cost of living statistics, the average UK house price was £284,691 in December 2023 (1.4% lower than the previous year).

Terraced properties in the UK saw the largest percentage decrease in their average price, dropping more than £9,000 in November 2023 compared to the same time in 2022. This represents a fall of 3.8%, compared to 0.7% for detached homes and 1.7% for semi-detached housing.

A breakdown of the average UK house by property type (November 2022-23)

| Property type | November 2022 | November 2023 | Difference (%) |

|---|---|---|---|

| Detached | £457,043 | £451,249 | -1.26% |

| Semi-detached | £281,749 | £277,880 | -1.40% |

| Terraced | £239,455 | £230,416 | -3.80% |

| Flat/maisonette | £231,945 | £225,652 | -2.70% |

| All | £291,092 | £284,321 | -2.30% |

(Source HM Land Registry)

Flats and maisonettes had the second-highest percentage decrease (2.7%) of all property types over the last 12 months. This equated to over £6,200 less in cost compared to the previous year.

UK mortgage arrears statistics and repossession stats 2022

According to the Financial Conduct Authority (FCA), at the end of Q3 2022, there were 87,930 mortgage loan accounts with arrears of more than 2.5% of the current loan balance. Of these, 15,670 had arrears of between 5% and 7.5%.

UK mortgage arrears statistics from UK Finance estimated that 630 homeowner properties were taken into possession in Q3 2023. This means that across the UK, on average, there were 6.8 properties repossessed every day between July and September 2023 – more than one every four hours.

Between July to September 2023, 45.5 daily mortgage possession claims, and over 10.5 mortgage possession orders, were made across England and Wales. In addition to this, an average of 271.1 landlord possession claims and 72.5 landlord possession orders were also made each day across the same period.

UK mortgage arrears statistics indicate that, at the end of October 2023, total mortgage debt stood at more than £1.63 trillion – £9 billion more than one year earlier. With almost 10.8 million households in the UK, this means the estimated average outstanding debt is £151,076 per household.

Want to know how much you’re eligible to borrow from mortgage lenders? Set your expectations by using our free mortgage calculator.

UK rental market statistics

According to UK rental market statistics from Zoopla, rental growth in the UK stood at 9.7% a year (as of December 2023) – well ahead of the inflation for wages, which was 6.5% in November 2023.

The UK has a distinct supply-demand issue when it comes to rented accommodation. Compared to the UK’s five-year average, UK rental market statistics indicate that demand for rental properties was down 11% in December 2023 from the previous year. However, this was still around a third higher than the average for the previous five years.

The stock of UK rental accommodation in 2022 is way below the five-year average. According to UK cost of living stats, the flow of new supply onto the market is around a fifth (18%) lower than the mean average figures for 2017-2022, but 20% higher than the same period last year.

The ONS rental index tracks growth across all rental homes. This is, on average, 6.2% more expensive in December 2023 compared to 12 months earlier. However, those moving to a newly rented property will find the rising cost of renting 8.3% higher than a year ago according to Rightmove. This is because rents for new lets reflect the current levels of supply and demand at the time of moving.

Seeing as the average renter moves every four years, and given the UK cost of living crisis, people may think twice about whether to find a new rental property or choose to stay put in their current one. This will amplify the squeeze on supply, and risk keeping the pressure on the UK rental market into 2025.

UK rental market statistics show that, over recent years, demand has reduced for two and three-bedroom houses, down to around 11% for each in 2022, whereas two-bedroom flats are up to more than a third (35%). The growth in demand for one-bedroom flats slowly grew between 2020 and 2022, from 30% to 32%.

According to our cost of living index, the UK ranks 12th best in the world when it comes to rent, monthly outgoings, and other associated living costs. The affordability of renting is broadly in line with the long-term average (LTA) since 2009. In Q2 2022, rent accounted for more than a third (34.4%) of earnings, compared to an LTA of 33%. This figure did drop to a low of 31.9% in Q1 2021 but has since slowly been on the rise, as the average price of rent continues to increase faster than the rate of pay.

Looking to buy your first home? Compare first-time buyer mortgage and help to buy mortgage rates from an array of lenders and find the best deal for you.

UK rental market statistics - private rent price increases in the UK

UK rental market statistics indicate that private rental prices in the UK were 6.2% higher in December 2023 compared to the same time in 2022 – the joint-largest annual increase in the previous six years alongside November 2023.

At the start of 2016, UK private rental charges were, on average, 2.6% higher than in January 2015, which then fell to 0.9% in July 2018. A period of steady increase with some fluctuations saw them reach 2.1% in January 2022, before rapidly increasing to 3% only six months later.

A breakdown of the change to UK average monthly rent for private properties between 2018 and 2023

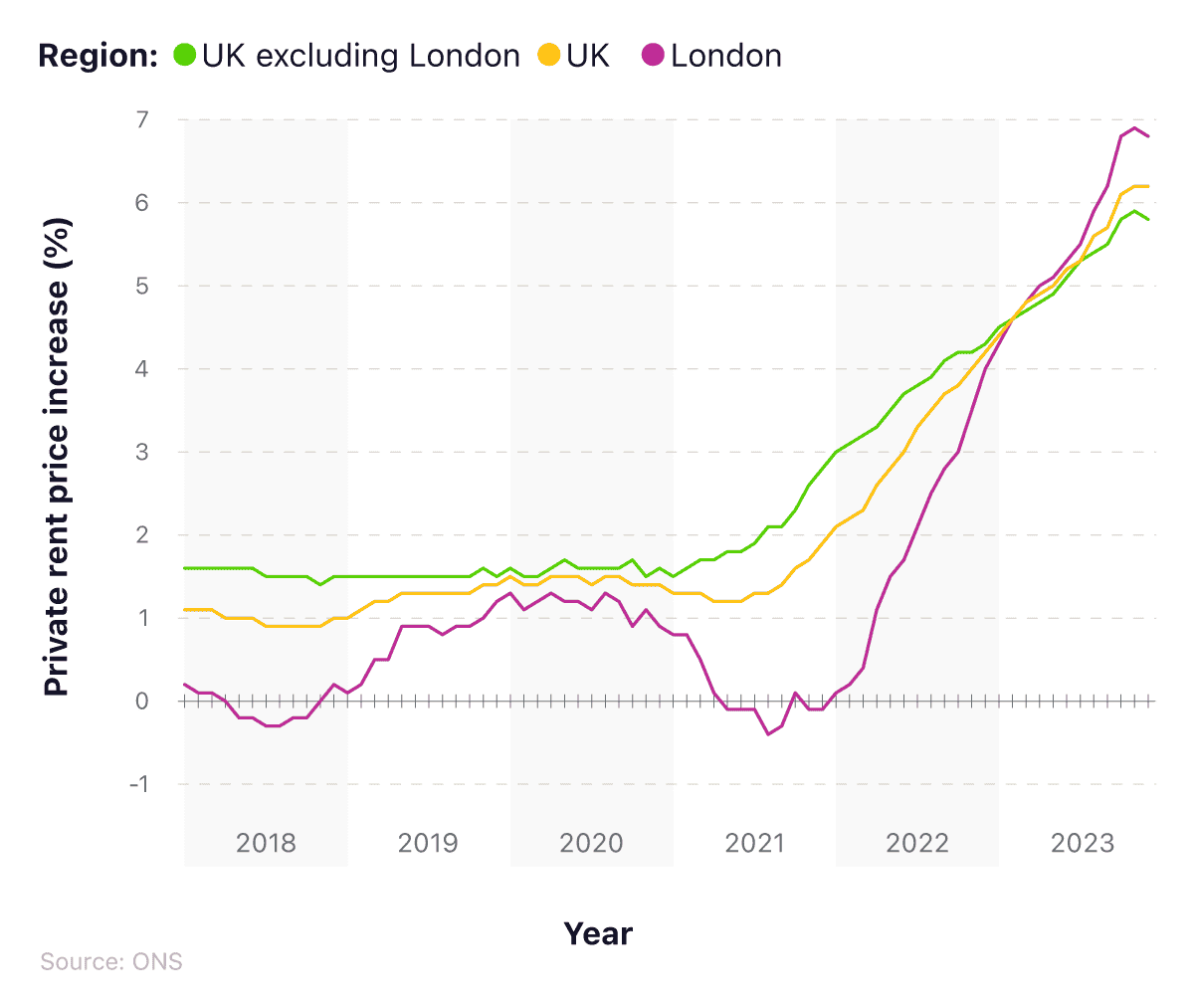

In London, the private rental market has been more volatile than the rest of the country, with the changes far more extreme over the given six-year period. In 2016, the average rental property in London was 3.9% higher than the previous year. This rate dropped dramatically in May 2018, when prices reached negative values for the first time in recent history (-0.2% compared to May 2017).

Following this, private rental prices have gradually increased and decreased between -0.3% and 1.3%. Since May 2022, the percentage change started to increase relatively quickly, reaching 2.1% in July 2022 compared to July 2021. In the second half of 2023, London’s annual price rises were consistently above the rest of the UK, peaking at 6.9% in November before falling to 6.8% in December.

When London is taken out of the UK national figures, the picture for private rental prices is more stable. UK cost of living statistics show that, throughout 2016 and 2018, there was very little change, with prices fluctuating between 1.4% and 2.3% higher compared to the previous 12 months. However, according to historic UK rental market statistics, the percentage change in private rent increased rapidly from 2.6% in November 2021 to 4.4% in January 2023. These increases continued throughout 2023, peaking at 5.9% in November before falling slightly in December (5.8%).

UK rental market statistics by region 2023

Between 2016 and 2022, all four UK nations witnessed a relatively similar pattern in the average cost of private rent, with fluctuating prices up until 2021, and a sustained increase throughout 2022 and 2023.

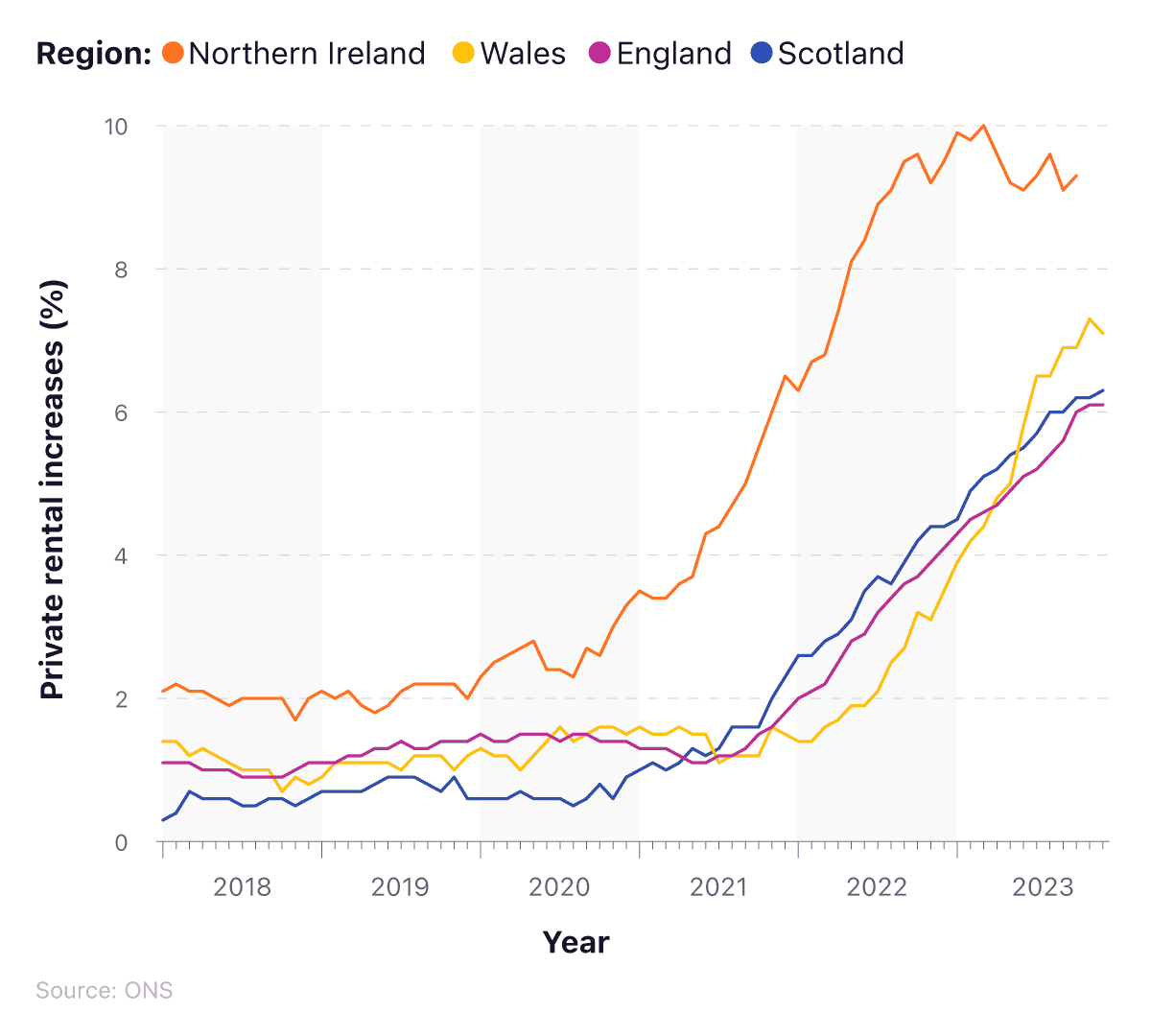

Throughout most of 2016 and 2017, the percentage change in private rental prices in England was higher than in the other three nations, despite falling from 2.8% in February 2016 to 1.6% in September 2017. After this point, Northern Ireland has sustained its position as the country with the highest rate of change in average rent prices in the UK.

Since January 2020, the rising cost of rent has been relatively significant in Northern Ireland, despite mild fluctuations between 2017 and 2019. As of October 2023, the percentage change stood at 9.3%, having been as high as 10% in March.

UK rental market statistics highlight that changes to private rental charges in England have been more gradual. After reaching a low of 0.9% in July 2018, it steadily rose and fell across the resulting three years. Since January 2022, it has trebled, rising from 2.0% to 6.1% as of December 2023 – the joint-highest increase on record in recent years.

A breakdown of changes to UK rental market statistics for different countries of the UK between 2018 and 2023

The private rental landscape for both Scotland and Wales is similar to that of England, but with some negative changes to note. For Scotland, the rate of change for private rental charges was 0.8% in January 2016, before dropping -0.2% in October later that year.

Between August 2016 and July 2017, the percentage change fluctuated above and below 0%, after which it gradually increased up until January 2021. Prices during this time alternated between 0.6% and 1.0%, compared to the previous year. From January 2021, there was a sustained increase, rising to a peak of 6.3% in December 2023.

For Wales, the initial picture for private rental costs is relatively similar to Scotland. Increases were felt between June 2016 and December 2017, when the average change in private rental charges went from -0.1% to 1.7% in December 2017. Things remained stable until 2022 when the figures began to rise dramatically.

By December 2023, UK rental market statistics show the average change in private rental charges in Wales stood at 7.1% – more than double the number recorded in December 2022 but a 0.2 percentage point fall from November 2023.

A breakdown of the rental affordability of different regions of the UK in 2023

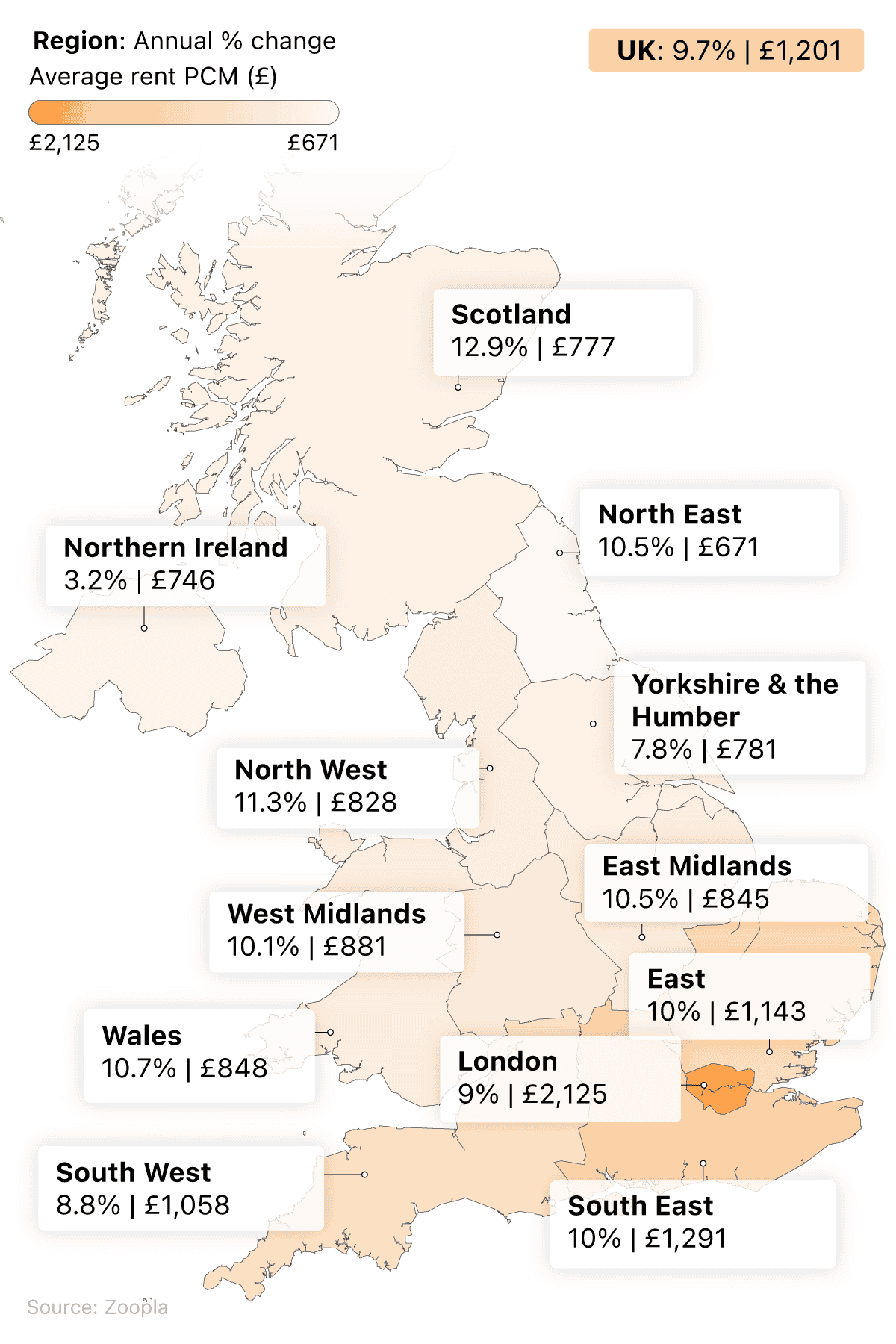

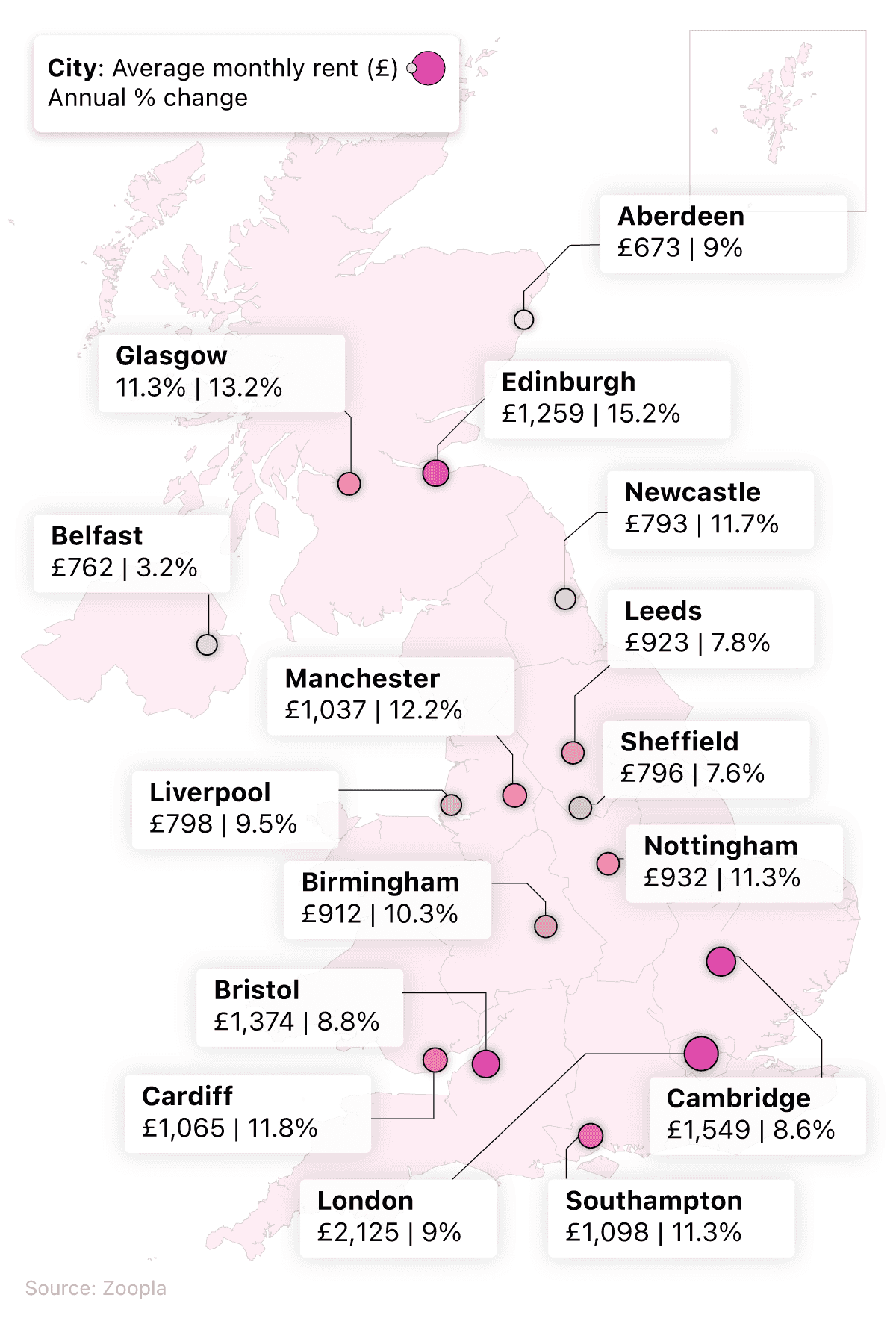

UK cost of living statistics indicate that, in 2023, London remained the most expensive place to rent in the UK, with average monthly costs of £2,125. This is more than three times as expensive as the North East (the UK’s cheapest rental location, at £671).

Our cost of living report found that the rising cost of rent made some areas such as Kensington and Chelsea average at almost £2,970 a month—the highest across anywhere in the UK.

Scotland recorded the highest year-on-year (YoY) growth for 2023 (12.9%), followed by the North West (11.3%). At the other end of the table, Yorkshire and the Humber’s YoY growth of 7.8% was the lowest figure recorded across the country.

The rising cost of rent doesn’t only affect England. Rent-affordability-by-region data shows that the average rent in Wales (£848 pcm) is nearly 10% higher than in Scotland (£777) and over 13% more than in Northern Ireland (£746).

A breakdown of the rent prices for the major UK cities in 2023

The UK has some of the best cities to move to for work. However, this is only beneficial if the associated wages of working there allow you to live the lifestyle you desire.

Data for 2023 average rental costs by region shows that London is the most expensive city to rent a property in the UK. At £2,125pcm, the rising cost of rent means renters here pay more than £575 a month more than second-placed Cambridge (£1,549), and around 316% more than the UK’s most affordable city, Aberdeen.

Edinburgh saw the largest growth in rental costs within the past 12 months, at 15.2%. By contrast, Belfast has seen the smallest growth, followed by Sheffield, at 3.2% and 7.6%, respectively.

If you are considering relocating for a better standard of living, check out our UK relocation report, which judges different places in the country on UK average house prices, salary, as well as environmental factors that may influence your overall quality of life by moving there.

Average UK council tax statistics 2023

In 2022-23, average UK council tax statistics showed that the cost for a typical Band D property was £1,996. This increased £99 (or 5.1%) for 2023-24, to £2,065 a year.

For other parts of the UK, the corresponding figures for a typical Band D property in 2023-24 are:

£1,789 in London (up from £1,684 in 2022-23)

£2,059 in metropolitan areas (rising from £1,960 in 2022-23)

£2,139 in unitary areas (rising from £2,036 in 2022-23)

£2,134 in shire areas (rising from £2,040 in 2022-23).

The UK’s average council tax costs will be £1,578 in 2023-24.

A breakdown of the most and least expensive places for UK council tax 2023-24

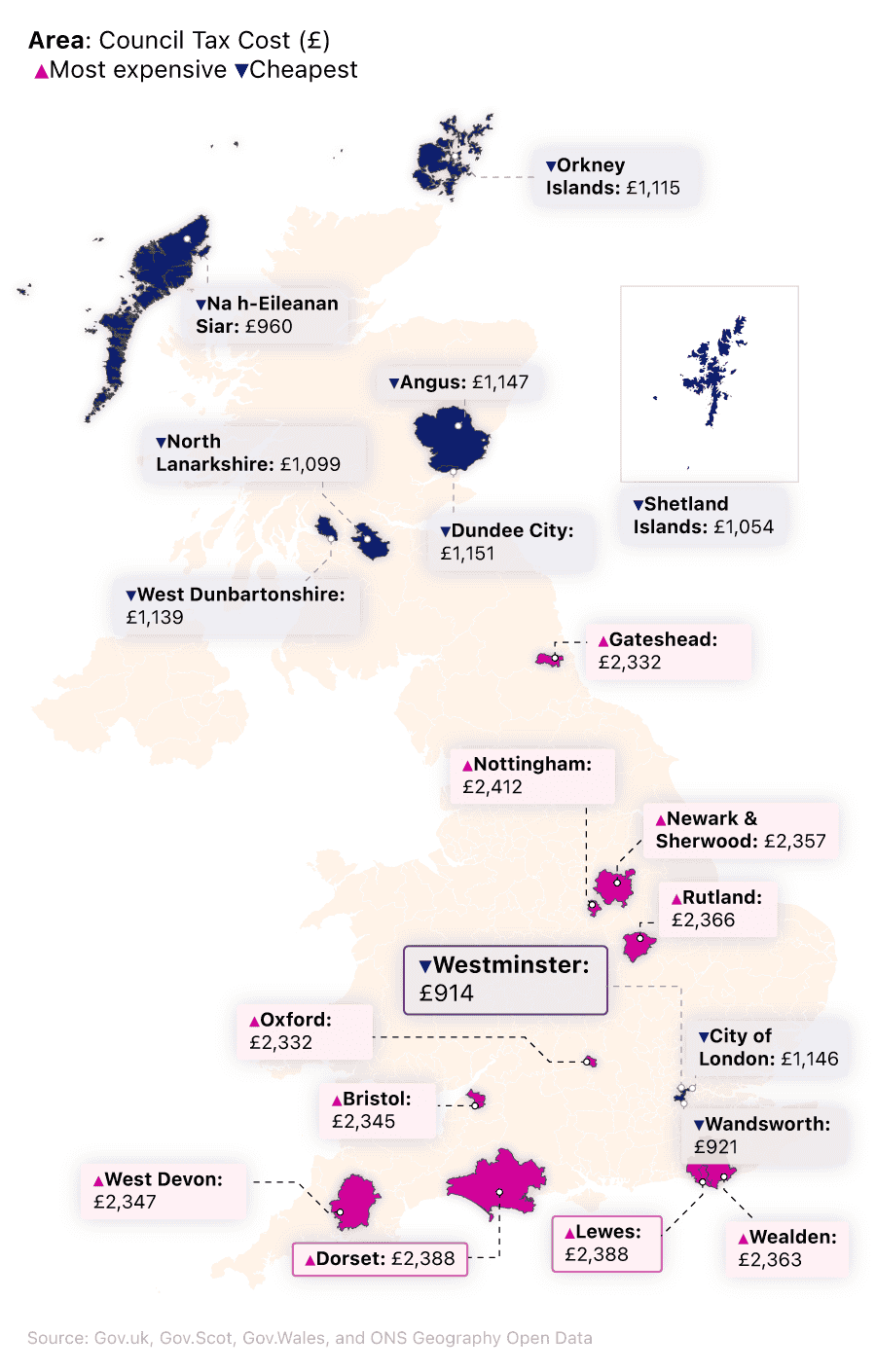

UK council tax statistics shows that the two cheapest areas for UK council tax in 2023 and 2024 can both be found in London. Council tax for residents of Westminster starts from as little as £914 a year, followed by Wandsworth at £921.

The most affordable location in Scotland is Na h-Eileanan Siar (£960), followed by the Shetland Islands (£1,054) – the third and fourth cheapest rates in the UK, respectively.

There is no Welsh representative in the top 10, with the lowest council tax in Wales (Caerphilly) more than £700 a year more expensive than Westminster.

England dominated the list of areas with the most expensive council tax, with all of the top 10 based in England. The two most expensive areas were both found in Nottinghamshire, with Rutland and the City of Nottingham having average annual rates of £2,366 and £2,412, respectively.

It’s not just about the annual cost of council tax, it’s what you get for your money. According to our study, the regions with the best return on their council tax are Wandsworth, Wigan, and Windsor & Maidenhead, when taking into account what services are offered by the council, such as emergency vehicle response times, education, and household recycling facilities.

UK council tax statistics for council tax support fund and housing benefits 2023

Our exclusive data analysed the budgets of each county council in England, with a focus on council tax support and household support funds. This data was then weighed up against the council’s reported population, giving an accurate figure of support available per head.

The main findings from our study show that:

Of the top 10 councils offering the most support, the top seven are all based in northern England.

Hartlepool offers the largest council tax support, with £3.78 per person available to its 92,000 inhabitants.

The City of London offers the least support per person regarding council tax, at just £0.79 (although that affects only 8,538 residents).

Population data reveals that Kent County Council has the largest population of all councils in England, being responsible for over 1.5 million people. The county features in 93rd place due to low council tax support and household support funds available.

A breakdown of England’s best and worst performing councils for council tax financial support

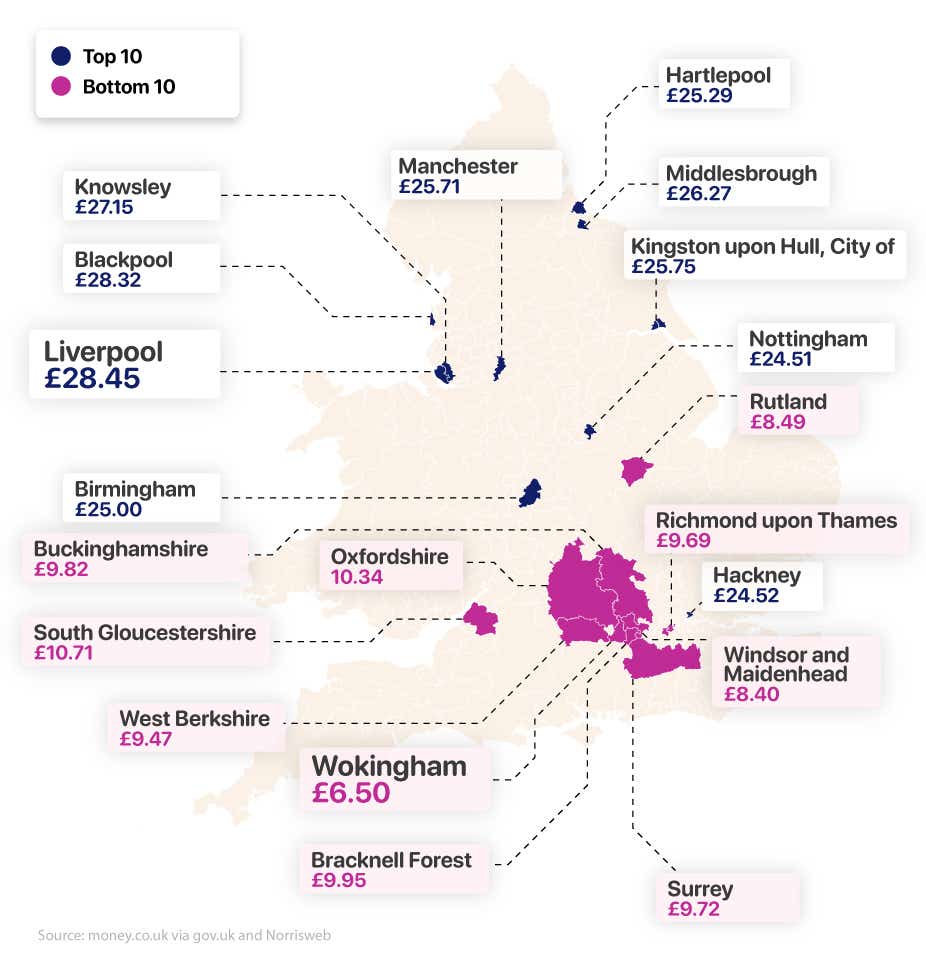

Data shows that Liverpool council offers the most support per person across their county. At £28.45 per head, Liverpool exceeds all other major cities in its household support fund, issuing £24.91 per person to those requiring assistance. Similarly, their council tax support fund is one of the highest in the UK, at £3.54 per person.

In the northwest of England, Blackpool offers marginally more per person than Liverpool in terms of council tax support (£3.57 vs £3.54, respectively). However, the same can’t be said for their household support fund, which offers £24.76 per person—15 pence less than that of Liverpool.

Overall, Blackpool’s combined support figure is £28.32 per head—13 pence less than that of Liverpool. However, that’s more than Knowsley (featuring in third on the list) which offers £27.15, a full £1.17 lower than Blackpool.

A breakdown of the UK’s highest performing councils for council tax financial support

| County council / unitary authority | Population | Number of households | Council tax support fund (£) | Household support fund (£) | Council tax support fund per capita (£) | Household support fund estimate per capita (£) | Support funding per capita (£) |

|---|---|---|---|---|---|---|---|

| Liverpool | 486,088 | 207,491 | 1,722,389 | 12,108,040 | 3.54 | 24.91 | 28.45 |

| Blackpool | 141,036 | 64,789 | 502,981 | 3,491,715 | 3.57 | 24.76 | 28.32 |

| Knowsley | 154,519 | 66,073 | 470,169 | 3,724,377 | 3.04 | 24.1 | 27.15 |

| Middlesbrough | 143,926 | 60,262 | 473,542 | 3,307,230 | 3.29 | 22.98 | 26.27 |

| Kingston upon Hull, City of | 267,014 | 115,472 | 798,075 | 6,076,587 | 2.99 | 22.76 | 25.75 |

| Manchester | 551,938 | 214,732 | 1,286,349 | 12,906,326 | 2.33 | 23.38 | 25.71 |

| Hartlepool | 92,338 | 40,930 | 348,937 | 1,986,043 | 3.78 | 21.51 | 25.29 |

| Birmingham | 1,144,919 | 423,456 | 3,035,699 | 25,582,270 | 2.65 | 22.34 | 25 |

| Hackney | 259,146 | 106,081 | 709,312 | 5,644,517 | 2.74 | 21.78 | 24.52 |

| Nottingham | 323,632 | 124,745 | 817,735 | 7,113,868 | 2.53 | 21.98 | 24.51 |

(Source: money.co.uk via gov.uk and Norrisweb)

Birmingham is the first council in the top 10 that isn’t in the north of England, listed in eighth place. With a population of over 1.1 million, the Midlands city has by far the largest population of any county council in the top 10. Their council tax support scheme is the lowest in the top 10, at £2.33 per person—a full £1.21 less than that of Liverpool.

Birmingham’s household support fund isn’t as large per person as that seen in the north of England, with £22.34 available to residents of the county. This makes it the highest council assistance package in the Midlands when it comes to council tax support (£25), but lower than that of northern, large metropolitan areas, such as Liverpool and Manchester.

A breakdown of the UK’s lowest performing councils for council tax financial support

| County council / unitary authority | Population | Number of households | Council tax support fund (£) | Household support fund (£) | Council tax support fund per capita (£) | Household support fund estimate per capita (£) | Support funding per capita (£) |

|---|---|---|---|---|---|---|---|

| Wokingham | 177,503 | 69,164 | 103,153 | 1,051,147 | 0.58 | 5.92 | 6.5 |

| Windsor and Maidenhead | 153,496 | 60,932 | 113,299 | 1,175,810 | 0.74 | 7.66 | 8.4 |

| Rutland | 41,049 | 16,694 | 33,919 | 314,742 | 0.83 | 7.67 | 8.49 |

| West Berkshire | 161,448 | 66,658 | 138,468 | 1,389,699 | 0.86 | 8.61 | 9.47 |

| Richmond upon Thames | 195,278 | 80,705 | 220,115 | 1,672,713 | 1.13 | 8.57 | 9.69 |

| Surrey | 1,203,110 | 481,818 | 1,111,933 | 10,581,659 | 0.92 | 8.8 | 9.72 |

| Buckinghamshire | 553,078 | 220,328 | 634,939 | 4,798,381 | 1.15 | 8.68 | 9.82 |

| Bracknell Forest | 124,607 | 50,248 | 128,690 | 1,110,936 | 1.03 | 8.92 | 9.95 |

| Oxfordshire | 725,291 | 288,108 | 778,230 | 6,722,512 | 1.07 | 9.27 | 10.34 |

| South Gloucestershire | 290,424 | 118,101 | 290,245 | 2,820,033 | 1 | 9.71 | 10.71 |

| Leicestershire | 712,369 | 296,408 | 759,096 | 7,240,078 | 1.07 | 10.16 | 11.23 |

(Source: money.co.uk via gov.uk and Norrisweb)

Wokingham, based in the county of Berkshire, offers the least council support for residents. With a population of 177,000, and a council tax support fund of just £103,153, the available help on offer is just £0.58 per person.

Similarly, with a household support fund of a little over £1 million, financial help is restricted to £5.92 per person—£1.74 lower than the fellow Berkshire county of Windsor and Maidenhead. The assistance package on offer from Wokingham County Council is £6.50 per head, which is £1.90 less per person than that of Windsor and Maidenhead.

Rutland County Council has the smallest number of residents of any area within the top or bottom 10, at just over 41,000 people. It also has one of the smallest council tax support budgets seen throughout England, at just under £34,000. This means the per capita tax relief is £0.83—£0.09 more than that of Windsor and Maidenhead.

Likewise, Rutland offers a one-pence increase for household support funds over Berkshire County, at £7.67. The overall assistance per head is £8.49—the third lowest offering throughout the nation.

Surrey has one of the largest populations in all of England’s counties, at a little over 1.2 million people. However, in terms of support on offer from their county council, Surrey comes in 147th out of 152 councils. Their budget of just £1.1 million for council tax support, and £10.5 million for household support, means help per person is £9.72 combined. Therefore, Surrey offers the lowest support for any county with a population of over one million people.

By comparison, neighbouring Hampshire, with a population of 1.4 million people, offers an assistance package of £11.29 per person, while Hertfordshire’s 1.2 million people can access £11.57 for both council tax and household support.

In terms of financial assistance, regarding both council tax and household support, there is a sharp divide between councils across the nation. Aside from outliers such as Hackney and Birmingham, the top 10 councils for financial support all hail from northern England, whereas the councils that offer the least are located in the south (besides Leicestershire and Rutland).

The disparity in terms of available funds is apparent too, with Wokingham’s £6.50 per head a full £21.95 less than that of Liverpool. Leeds, one of the largest cities in the north of England, has £19.53 available per person, whereas York, only a 45-minute drive away, offers just £11.27.

Average salary vs cost of living UK 2023

According to the cost of living statistics from the Joseph Rowntree Foundation, a single person living in the UK in 2023 needed to earn at least £29,500 to reach a minimum, acceptable standard of living. For a couple with two children, this increases to an average combined income of around £50,000.

However, these figures will vary depending on which part of the country you live in, your age, and how many dependents (i.e. children) you have.

Using the Minimum Income Calculator tool, we calculated the least amount of money you need to earn each year to achieve a decent standard of living. Below is a series of tables depicting different living arrangements and scenarios, plus the minimum amount of income needed to sustain a reasonable standard of living in that area.

The average cost of living in the UK by household type - one-person household

| Scenario | Location | Earnings | Net income (per week) |

|---|---|---|---|

| Single person, under the age of 65, living alone with no children | Inner London | £48,035 | £703.84 |

| Outer London | Outer London | £43,889 | |

| Scotland | Scotland | £29,568 | |

| Rest of UK (not London or Scotland) | Rest of UK (not London or Scotland) | £29,541 |

(Source: Minimum Income Calculator UK)

As a single person living in the UK outside of London and Scotland, you will need to earn around £29,541 a year to have a comfortable standard of living. This will give you a weekly income of just under £441 to spend on essential items, such as food, utility bills, and accommodation. These figures are similar for Scotland (£29,568).

However, if you move to London, these figures change considerably. Should you choose to live in Inner London, you’ll need to earn in excess of £48,000 a year to have a decent standard of living, as your expenses could set you back approximately £704 a week. Outer London is slightly more affordable, requiring earnings of £43,889, and more than £450 a week in living costs.

The average cost of living in the UK by household type - single-family households

For a single-parent household, the required salary for a decent standard of living can vary considerably, depending on where you live in the country, how many children you have, and how old they are.

| Scenario | Location | Earnings | Net income (per week) |

|---|---|---|---|

| Single person, under the age of 65, living alone with one child (under the age of one) | Inner London | £63,498 | £959.57 |

| Outer London | Outer London | £71,705 | |

| Scotland | Scotland | £37,267 | |

| Rest of UK (not London or Scotland) | Rest of UK (not London or Scotland) | £41,733 |

(Source: Minimum Income Calculator UK)

UK cost of living stats for a single parent, under the age of 65, living in inner London with a child under the age of one, suggest their annual earnings would need to exceed £63,498 to live comfortably, compared to £71,705 in outer London. By comparison, the same family set up in Scotland would require less than two-thirds of this amount (£37,267), with the cost standing at more than £41,733 for the rest of the UK.

| Scenario | Location | Earnings | Net income (per week) |

|---|---|---|---|

| Single person, under the age of 65, living alone with two children (one of primary school age and one of secondary school age) | Inner London | £44,979 | £874.98 |

| Outer London | Outer London | £47,598 | |

| Scotland | Scotland | £60,424 | |

| Rest of UK (not London or Scotland) | Rest of UK (not London or Scotland) | £49,411 |

(Source: Minimum Income Calculator UK)

Being a single parent with a young child was one of the more expensive scenarios in 2023. By contrast, a single parent with two children (both of school age), saw their required earnings drop to £44,979 for inner London, and just under £48,000 for outer London. This left about £875 and £906 a week, respectively, to live comfortably.

By comparison, the earnings required in Scotland were greater than in London (at approximately £60,424 a year) and just over £49,400 for the rest of the UK. Both of these could give you just over £820 a week to live on, and comfortably support yourself and two children.

While it’s possible to cut the cost of living alone, how much you are bringing in each month is a major deciding factor as to how you coped during the UK cost of living crisis in 2023. These pressures certainly become slightly easier when you introduce a second person (and income) into the equation.

The average cost of living in the UK by household type - coupled, family households

Living as a couple with children will take off some of the pressure, as it is likely you will have two incomes as well as help with childcare. However, for both inner and outer London, a family’s cost of living is considerably higher than in other parts of the UK, with required household earnings of £70,423 and £81,031 a year, respectively for couples with a child under the age of one. Such an income could provide them with between £1,100 and £1,200 to live on each week.

| Scenario | Location | Earnings (joint) | Net income (per week) |

|---|---|---|---|

| Couple, under the age of 65, living together with one child (under the age of one) | Inner London | £70,423 | £1,114.85 |

| Outer London | Outer London | £81,031 | |

| Scotland | Scotland | £44,418 | |

| Rest of UK (not London or Scotland) | Rest of UK (not London or Scotland) | £49,103 |

(Source: Minimum Income Calculator UK)

UK cost of living statistics show that, for those in Scotland, the required annual salary drops by more than a third, to just above £44,400, and about £49,100 for the rest of the UK. This could result in couples having around £946 a week to support themselves and their young child.

| Scenario | Location | Earnings (joint) | Net income (per week) |

|---|---|---|---|

| Couple, under the age of 65, living together with two children (one primary school age and one secondary school age) | Inner London | £57.38 | £1,028.75 |

| Outer London | Outer London | £62,604 | |

| Scotland | Scotland | £55,963 | |

| Rest of UK (not London or Scotland) | Rest of UK (not London or Scotland) | £55,959 |

(Source: Minimum Income Calculator UK)

For a couple with two children of school age, the joint earnings required for a good standard of living is reduced by almost a third for inner London, at a little more than £57,300. For outer London, this figure is almost £63,000. This could supply families with almost £1028.75 and £1073.56 a week, respectively, on which to raise their family and comfortably provide for them.

For Scotland and the rest of the UK, the annual combined earnings required for the same scenario drops to just under £56,000, resulting in just under £943 a week for living expenses in these two areas.

Average cost of living in the UK by household type - retired households

For retired households in the UK, the loss of annual earnings from employment is replaced with a pension, whether that be a state pension, a private pension scheme (such as a self-invested personal pension, or SIPP) or a workplace pension. Most older residents will not have the pressure of providing for their dependents or paying a mortgage by the time they reach retirement age, and therefore the required amount of money needed for a decent standard of living drops significantly, compared to those of working age.

| Scenario | Location | Pension | Net income (per week) |

|---|---|---|---|

| Single person, 65+, living alone with no dependents | Inner London | £25,331 | £440.70 |

| Outer London | Outer London | £25,047 | |

| Scotland | Scotland | £20,453 | |

| Rest of UK (not London or Scotland) | Rest of UK (not London or Scotland) | £20,480 |

(Source: Minimum Income Calculator UK)

UK cost of living stats for a single person aged 65+, and living on their own in inner London, suggest they may need a pension or other earnings of at least £25,331 a year for a decent standard of living. This would give them just over £440 a week to live on. For outer London, the corresponding figure drops by around £300, to just over £25,000, and dips below £20,500 for Scotland and the rest of the UK.

| Scenario | Location | Pension | Net income (per week) |

|---|---|---|---|

| Couple, 65+, living together with no dependents | Inner London | £34,294 | £626.42 |

| Outer London | Outer London | £33,964 | |

| Scotland | Scotland | £27,820 | |

| Rest of UK (not London or Scotland) | Rest of UK (not London or Scotland) | £27,854 |

(Source: Minimum Income Calculator UK)

By contrast, couples aged 65+ and living together with no dependents in inner London may need to have a combined pension of almost £34,300 (about £626 a week) to sustain a decent standard of living. This drops to around £33,964 for outer London (approximately £621 a week to cover living expenses).

For the rest of the UK and Scotland, the combined pension needed is a little more than £27,800 a year, providing them with approximately £527 a week to buy food, pay bills, and live well.

See if you could save money on pension fees by comparing deals from leading pension transfer providers.

The cost of living by household type - average weekly expenditure UK, April 2023

The Minimum Income Standard (MIS) is based on specific budgets, calculated for a range of households and individuals. The table above sets out the budgets for four household types, broken down into various categories of spending.

Since 2022, the MIS has risen considerably for all four groups, increasing by 12.5% for single, working adults and more than 12.3% for pensioner couples. Lone parents with two children have seen the smallest rise, at just under 11%. Adult couples with two children saw their cost of living rise by almost 11.1% in the 12 months to April 2023.

| Category | Single adult, working age | Couple, pensioners | Lone parent with two children (aged 2-4 and primary age) | Couple, two children (aged 2-4 and primary age) |

|---|---|---|---|---|

| Food | £77.21 | £113.36 | £105.21 | £144.86 |

| Alcohol | £8.97 | £12.99 | £5.88 | £11.41 |

| Clothing | £14.99 | £19.03 | £41.50 | £51.16 |

| Water rates | £8.06 | £9.51 | £12.53 | £12.54 |

| Council tax | £20.68 | £27.58 | £24.13 | £32.17 |

| Household insurance | £1.75 | £1.99 | £1.73 | £1.93 |

| Fuel | £40.15 | £43.44 | £58.64 | £61.95 |

| Decorating and maintenance | £2.01 | £2.01 | £2.19 | £2.19 |

| Household goods | £15.83 | £24.43 | £33.06 | £34.08 |

| Household services | £8.93 | £13.24 | £15.02 | £11.07 |